World of Extremes

April 21, 2024

***************

When I worked on the floor of the CME in eurodollars, there was a guy that had started at the Citi desk. Slight of build, sandy colored hair, ordinary looking. His standout feature was that he was prone to embellishing his accomplishments and intellectual acumen. This being the floor, one of his coworkers created a CV for him with a list of outrageous claims. Of course, everyone jumped in and added bullet points with stuff like this (it was a long list):

Taught Myron Scholes option math

Ran the Boston Marathon in two hours

Received a patent for a perpetual motion machine

and, one of my favorites:

Invented fire

Ruthlessly funny. I don’t know what happened to that guy, but I don’t think he lasted on the floor for long. Probably in Congress. Of course, I don’t think he ever went so far as to suggest his relatives were eaten by cannibals; that’s at another level.

We’re in a world of extremes dominated by outrageous hyperbole. A tired refrain from market pundits is often, “This won’t end well.” Look, it’s ALWAYS not ending well for someone out there. And even the bad stuff is usually good for someone. Let’s try to get on that side.

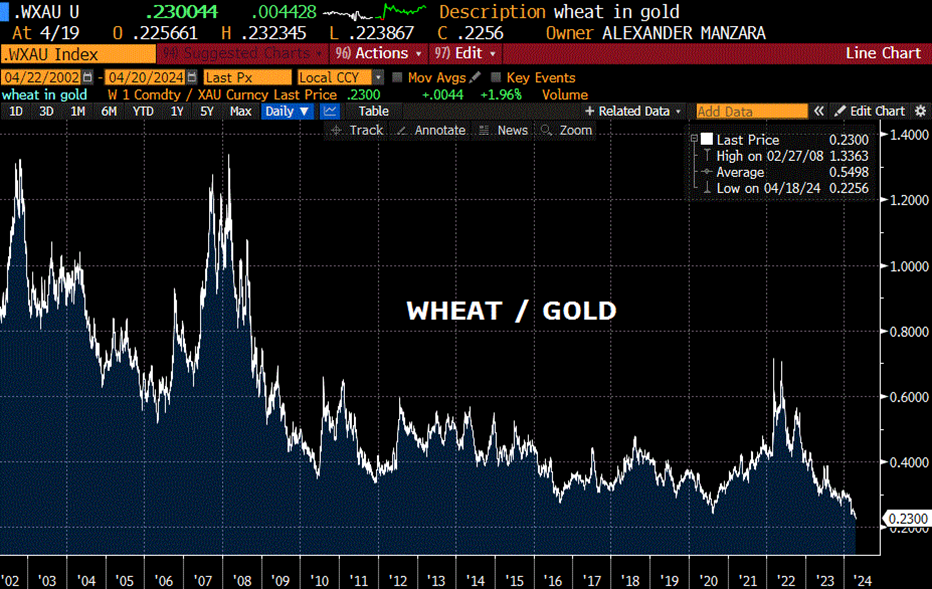

I’ve become somewhat obsessed with the prices of grains denominated in gold. Wheat priced in gold is at its lowest EVER. But there are a lot of relationships that seem extremely stretched and stressed, not just political. Russell 2k divided by Nasdaq Comp is near its absolute low. Oil priced in gold is compressed. The 2/10 treasury spread reached its lowest level since the 1980s last year (-108, now -36), and has been inverted for over seven quarters, almost the longest period in history. The BBB spread to treasuries is 117 according to the St Louis Fed site; close to its lowest level since 2000 (107).

Emerging mkt currencies are under pressure vs USD. The Indonesian rupiah and Malaysian ringgit have fallen to Asian Crisis (late 1990’s) levels. The Indian rupee made a new low this week, consistently weakening against USD. Same with the Vietnamese Dong; it has collapsed from 24270 to 25430 (17%) this year. $/yen is at its highest level since 1990.

US debt to GDP is over 120% and increasing again. It had hit 133% during covid but was below 65 for most of the period before the GFC.

Below are wheat and oil priced in gold since 2002. I am guessing that these charts might even be slightly more dramatic were it not for the advent of bitcoin, which likely siphoned off a bit of the ‘safe and easily portable store of value’ from gold, if only at the margin.

The next chart is Russell 2k divided by the Nasdaq Composite. I’ve included Fed easing periods which may have nothing to do with the equity index ratio, I only wanted to highlight how quickly the Fed has been inclined to cut the funding rate when stress shows up. The parallel to today might be the dotcom bubble as the calendar rolled into 2000. The Fed didn’t reduce rates right away, but when it did start cutting in January 2001 it went in a hurry. Same for the GFC.

The promise of new technology to increase productivity should benefit Russell companies as well. That was the same dynamic as in the late 1990’s of course, but it resolved with the Nasdaq crash. We experienced a tiny taste of that on Friday, with CCMP -2.05% and Russell +0.24%.

The SOFR curve has been squeezing out the prospect of easing in 2024, belatedly guided by Federal Reserve officials (in a flip from the December pivot). The lowest quarterly contract on the strip is SFRM4 at 9474 or 5.26%, close to the current Fed Effective of 5.33%. The peak contract on the strip is SFRU7 at 9595.5 or 4.045%. The difference between low to high is just 121.5 bps over three years. Most of that difference is contained in the next two years, for example, SFRM4/SFRM6 spread is -107.5 (9474/9581.5). You can see on the chart that recent easing episodes took less time than two years and are of 2x to 5x greater magnitude than M4/M6.

Does it have to play out that way this time. Nope. But it might.

In terms of inflation, we get PCE prices on Friday. Month/month expected 0.3 for both headline and core, same as last month. Year/year headline expected 2.6 from 2.5 and Core 2.7 from 2.8. My sense is that inflation remains sticky, but trending lower. I think there are both upside and downside risks. Regarding AI, I saw this twitter quote: “Imagine we discovered a new continent with 100 billion people and they’re all willing to work for free! That’s what’s about to happen with AI…” A stretch? I think so. But I also saw a clip from Goldman hypothesizing that the gap between GDP and GDI is due to immigration: “An undercounting of unauthorized immigration has likely contributed modestly to the sharp increase in the gap between GDP and GDI over the last year. We suspect that GDP which is an expenditure-based measure…may have captured the consumption boost from the recent immigration surge, while GDI which is income-based, may have underestimated total employment and compensation paid to undocumented workers…” There’s a much more prosaic reason that inflation may be contained: new immigrants are being paid much less under the table to work. The pressure to incorporate new entrants legally into the workforce is only going to grow as fiscal largesse runs into a brick wall. That brick wall comes in the form of higher rates at the long end of the treasury curve.

Treasury auctions of 2s, 5s and 7s this week. May 1 is both the FOMC and the Treasury’s Quarterly Refunding Announcement. Thankfully, we’re in the blackout period for Fed speakers. Bonds continue to trade heavy. If Yellen were to weight issuance to the front end again (like November) then USD will further strengthen against EM and hasten a crisis.

Interesting thesis by Gavekal (I think I’m summarizing correctly). In an environment of fiscal dominance, bonds are no longer a safety anchor for a portfolio. They will go down with stocks. Rather, real assets (like gold) should comprise about 30-35% of one’s portfolio as a safe anchor.

| 4/12/2024 | 4/19/2024 | chg | ||

| UST 2Y | 488.0 | 496.9 | 8.9 | wi 495.0 |

| UST 5Y | 453.1 | 465.6 | 12.5 | wi 464.8 |

| UST 10Y | 449.7 | 461.2 | 11.5 | |

| UST 30Y | 460.1 | 470.9 | 10.8 | |

| GERM 2Y | 285.6 | 300.0 | 14.4 | |

| GERM 10Y | 235.9 | 250.0 | 14.1 | |

| JPN 20Y | 162.6 | 160.1 | -2.5 | |

| CHINA 10Y | 228.4 | 225.6 | -2.8 | |

| SOFR M4/M5 | -76.0 | -68.0 | 8.0 | |

| SOFR M5/M6 | -42.5 | -39.5 | 3.0 | |

| SOFR M6/M7 | -14.0 | -13.0 | 1.0 | |

| EUR | 106.44 | 106.55 | 0.11 | |

| CRUDE (CLM4) | 85.08 | 82.22 | -2.86 | |

| SPX | 5123.41 | 4967.23 | -156.18 | -3.0% |

| VIX | 17.31 | 18.71 | 1.40 | |