To start the week…

Oct 7, 2019

–In spite of a spirited 40 point rally in ES on Friday, (Nasdaq and SPX both up 1.4%), yields remain close to recent all time lows. Tens fell 2.2 bps to 1.507%, and that’s in the face of this week’s supply of 3, 10 and 30 year paper. In response to new highs in the curve on Thursday, a decent amount of flattening trades went through on Friday, bringing 2/10 down 2.8 bps to 11.9. This morning stock futures have given back some of Friday’s gain, as China reportedly wants to narrow the focus on a trade deal, and N Korea talks hit an impasse. Additionally, Bernie Sanders’ health scare was upgraded to a heart attack; one poll showed that his supporters would migrate primarily to Warren, leaving her as front runner.

–Record low unemployment rate of 3.5% (since 1969) reported on Friday, but wage growth decelerated to 2.9%. This week we’ll get inflation data in the form of PPI on Tuesday and CPI Thursday, with the Fed minutes in between on Wednesday afternoon. Just over three weeks until the Oct 30 FOMC, and spreads indicate that odds of an ease are > 70% as Oct/Nov FF spread settled -17.75. Also worth noting that EDZ9/EDH0 edged to a new low of -36.0 on Friday (-0.5). This partially reflects weakness in EDZ9 due to turn-of-year considerations, and also the idea of front-loaded easing. With EDZ9/EDZ0 at -57.5, Z9/H0 comprises nearly 2/3rds. EDH0/EDZ0 9-month spread is only -21.5.

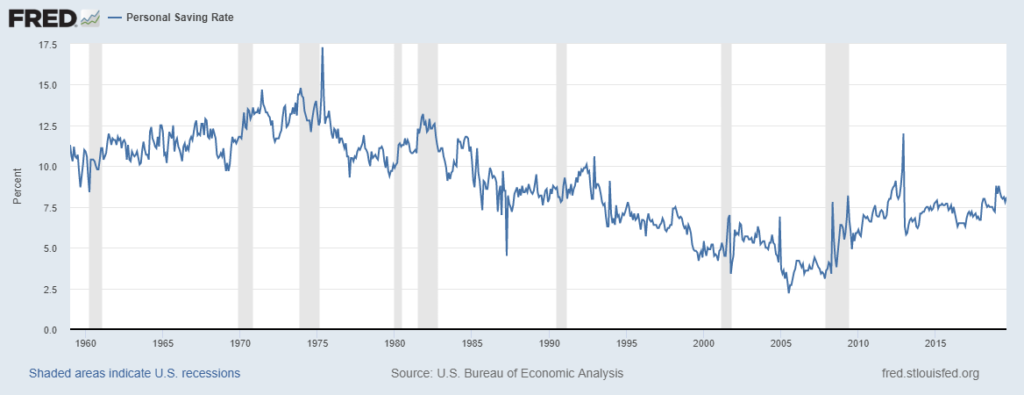

–The ‘real’ ten year yield as shown by the inflation-indexed note is again zero. Not exactly a sign of a robust economy. One other interesting note: An article on CNBC blames millennials for – get this _ a high savings rate! https://www.cnbc.com/2019/10/06/millennials-are-to-blame-for-sluggish-economy-raymond-james-report.html

While I don’t know that I agree with the premise, I did go to the Fed website to get a chart of the savings rate (attached), and sure enough it’s over 8%.