The ‘Countertrade’

February 23, 2025 – Weekly comment

*******************

Fascinating story on slashgear.com about Pepsi’s dealings with the old Soviet economy.

Here are a few snippets:

To solve this problem, Pepsi orchestrated what is known as a “countertrade,” essentially allowing the Soviets to pay for Pepsi sodas with a commodity rather than cash. Bartering agreements were a common practice for the USSR in its international business deals in 1971. For example, even the Swedish band ABBA would receive its royalty checks in the form of oil and food goods.

So what did the Russians offer Pepsi in this initial venture? A drink of their own, vodka. As such, Pepsi became the official U.S. importer and distributor of Stolichnaya Vodka, making it the first company to bring authentic Russian vodka stateside since Prohibition.

Later, the deal became larger and more complicated:

Partnering with two Norwegian companies, Pepsi Co. traded for 85 Russian oil tankers worth nearly $2.6 billion —roughly $82 billion in today’s currency. The Norwegians facilitated the deal by scrapping the military vessels and leasing the tankers for their Cola partners. The Soviet Union, in turn, increased its Pepsi bottling locations to 50, and saw an overhaul of its shipyards. As Kendall put it during a company press conference, it was “the largest and most wide-reaching agreement ever signed in the field of consumer goods.”

When the Soviet Union collapsed in December 1991, it took much of [CEO] Kendall’s deal with it.

…Looking back, Kendall described it thus: “We had a multibillion-dollar contract with a nonexisting entity — the Soviet Union.”

Read More: https://www.slashgear.com/1778945/pepsi-navy-fleet-russian-submarines/

Archaic vestiges of another time. But then I saw this post on X:

Boeing is returning to Russia, they need titanium…

The company is going to allow Russian airlines to purchase aircraft and establish supplies of spare parts to the domestic market, and in return receive titanium from Russia.

You might have thought that the title of this piece, Countertrade, has to do with macro themes in the futures markets. And it does; we’ll get to that. But the stories above also have everything to do with the creativity of capitalism and markets: Dealmaking. Credit risk. Supply chain risk.

The over-arching theme reminds me of a speech given by the fiery former CME Chairman Jack Sandner at an annual meeting. “The CME isn’t a ‘trading’ business. It’s bigger. OUR business is “RISK MANAGEMENT”. (At the time the exchange was owned by member firms and members).

When we think ‘risk management’ we tend to think ‘insurance’. And if there’s one thing that has contributed to inflation and forward expectations thereof, it’s retail insurance for homes and cars. Yet, in the macro markets they’ve been giving premium away cheap. In last weekend’s piece I referred to the low level of the MOVE index at 84.57 and noted that VIX was scraping along the lows at 14.77. Kevin Muir (MacroTourist) reported last week that FX vol has been in the dirt. Well, we got a bit of a ‘countertrade’ this week with MOVE up to 91.83 and VIX up to 18.21.

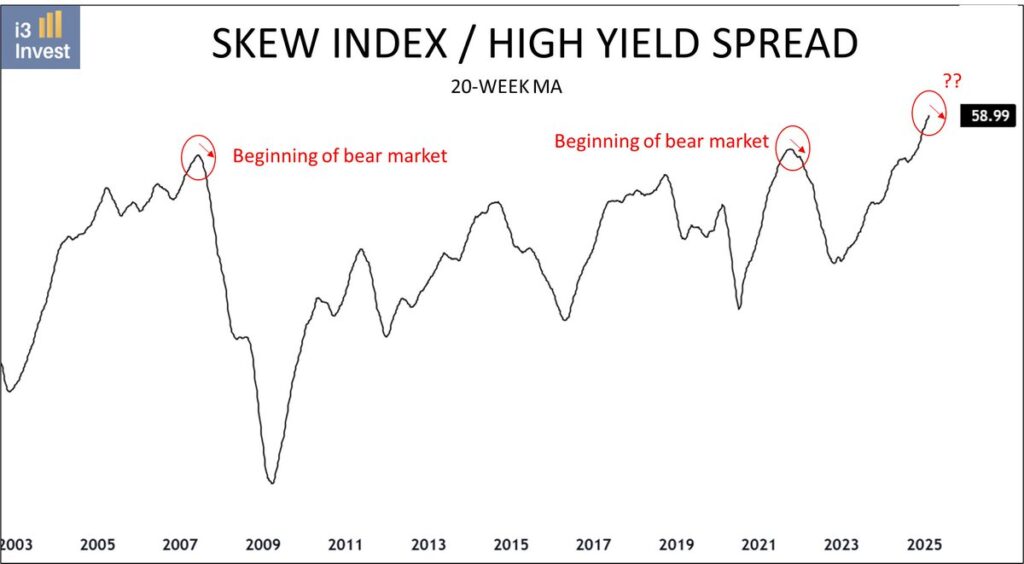

There was an interesting X post Friday by Guilherme Tavares @i3_invest

The ratio between SKEW and Credit Spreads has reached its highest level ever.

In the past, similar high levels haven’t been favorable for equities. A high Skew Index suggests options traders are worried about a potential sharp decline in equity markets (tail risk). A narrow high-yield spread, however, indicates that the bond market isn’t yet pricing in significant credit risk or economic deterioration.

Who is the dumb money here?

I didn’t attempt to recreate this chart or verify the data, but intuitively it makes sense. As a sidebar, I refer to the etf HYG (high-yield). In late July’s yen-carry debacle, HYG had a brief, sharp, sell-off. Currently it’s near the high but has not been making new highs recently with SPX.

From a site called marketchameleon.com “…put open interest [of 5.0 million in HYG] has risen 11.9% in the last 5 days. Compared to its 52-wk avg of 4.5 million contracts, the current put open interest for HYG is higher than usual.” In the interest of FULL DISCLOSURE, I am personally long puts on HYG. This is NOT INVESTMENT advice. I’m just dabbling. But it may be worth noting that the yen is strengthening in similar magnitude to the mid-July move.

I can’t quantify the risks, but there seems to be a lot of dangling uncertainties piling up in the last week or so. The previous week’s repudiation of the high CPI print (TY completely erased the CPI sell-off the next day) was a tell. Then, the FOMC minutes revealed a possible ‘pause’ of balance sheet run-off, potentially removing a weight on treasuries. There’s a bit more press about Norinchukin’s unrealized losses. Friday there was a new corona-virus headline. Are any of these things ‘real’ enough to spark Fed easing? Maybe not, but when taken all together, it’s not a big stretch to say that interest rate futures and options seemed a bit cheap. The market already ignored CPI. So, pay 9571 for FFK5, risking 4 to make 21? (or 15.5 if skip March and go in May) Why not? (Buyer of 110k Thursday afternoon at 9571, settled 9574 on Fri). Load up on SFRU5 9625 calls vs futures? Why not. (Since Thursday, new buyer of over 100k from 10 to 11.5, settled 14.75 vs U5 at 9601.5).

I would mention one other thing that caught my interest. I listened to a Jeffrey Gundlach interview with Tony Robbins from Feb 11. Gundlach mentioned that he is only buying treasuries with coupons at 1% or lower. The reason: he’s concerned about a cram-down. Paraphrasing: “…what if the gov’t says that every bond with a coupon above some hypothetical, call it 1%, is now legally changed to just 1%? That is, a 7% coupon bond turns into 1%. So if you own 7s and wake up tomorrow and the coupon is 1, you’re down about 80% in price.” Now, this might be an extreme. But there are obviously a lot of out-of-the-box ideas being discussed at high levels, in order to avoid the debt-spiral trap. Iron-clad deals occasionally change, as Kendal discovered with the Soviet Union.

https://www.youtube.com/watch?v=rYCiwwSjmFY

Another DoubleLine hypothetical last week questioned whether MSFT debt is ‘safer’ than that of the US gov’t. Related to that, from @CapitalJurassic:

Rumor going around that $MSFT is paying penalties to get out of some data center contracts & power agreements– changing tone drastically on CAPEX growth. Might be another DeepSeek shockwave to the semi supply chain.

Another uncertainty. I suppose the takeaway from all of this is: Question your assumptions. Like the 1960s catchphrase ‘Question Authority’.

No Coke. Pepsi.

Note record level of OI in FV, TY and UXY futures as H/M rolls are in full swing.

| 2/14/2025 | 2/21/2025 | chg | ||

| UST 2Y | 425.5 | 419.0 | -6.5 | wi 418.5 |

| UST 5Y | 432.7 | 425.7 | -7.0 | wi 425.2 |

| UST 10Y | 447.4 | 441.6 | -5.8 | |

| UST 30Y | 469.4 | 466.6 | -2.8 | |

| GERM 2Y | 211.3 | 210.2 | -1.1 | |

| GERM 10Y | 243.1 | 247.0 | 3.9 | |

| JPN 20Y | 201.3 | 205.3 | 4.0 | |

| CHINA 10Y | 165.0 | 175.0 | 10.0 | |

| SOFR H5/H6 | -36.8 | -43.8 | -7.0 | |

| SOFR H6/H7 | -1.0 | -1.0 | 0.0 | |

| SOFR H7/H8 | 5.5 | 7.5 | 2.0 | |

| EUR | 104.93 | 104.60 | -0.33 | |

| CRUDE (CLJ5) | 70.71 | 70.40 | -0.31 | |

| SPX | 6114.63 | 6013.13 | -101.50 | -1.7% |

| VIX | 14.77 | 18.21 | 3.44 | |

| MOVE | 84.67 | 91.83 | 7.16 | |

https://uk.finance.yahoo.com/news/abba-music-soviet-oil-world-143000023.html