The Bell Tolls

June 2, 2024 – Weekly Comment

**********************************

In March 2007, an article in the WSJ cited problems at Bear Stearns’ subprime mortgage funds. In June 2007 Bear pledged a collateralized loan of around $3.2B to its sinking funds, the High Grade Structured Credit Strategies Fund and the Credit Enhanced Leverage Fund. By July 17, 2007, Bear reported that both funds were essentially worthless. They were ringing the bell.

A contemporary paper on that era’s credit crisis noted, “In the summer of 2006, it became clear that the subprime mortgage market was in stress. At this time, the ratings agencies issued warnings… Moody’s first took rating action on 2006 vintage subprime loans in Nov 2006.”

After a spirited 13% rally in 2H 2006, SPX pulled back in March ’07. Having ended 2006 at 1418, by July 13 it was 1552. A hard sell-off ensued on the ‘worthless’ news, but by October’07 SPX made a new high of 1576, as the Fed had cut 50 bps in September, from 5.25% to 4.75%. By the end of January 2008, FF had been slashed to 3% as stocks cratered. Incidentally, CPI was 3.4% in March 2006 (same as now) and peaked at 4.3% in June 2006. Thus began what is called the Great Financial Crisis.

Last Wednesday, Jamie Dimon said “There could be hell to pay” regarding private credit. “I’ve seen a couple of these deals that were rated by a rating agency and, I have to confess, it shocked me…”

Right on cue, BBG reported Friday: “Canadian investment mgr Ninepoint Partners is temporarily suspending cash distributions in three of its private credit funds, making it the latest lender to put a squeeze on investors to cope with a liquidity crunch.”

The largest of the three funds is Ninepoint-TEC, which reported C$1.2 billion in assets under management at the end of 2023. It makes asset-backed loans to companies that “may have difficulty obtaining financing from other sources” — and certain borrowers have the option of using a payment-in-kind structure rather than cash interest payments…So-called PIK loans allow a company to defer some or all interest payments until the debt matures.

The Ninepoint Alternative Income Fund, which has about C$600 million in AUM, has the bulk of its loans to middle-market companies in the U.S. and Canada. It normally targets payouts to investors of 10% to 12% of the average NAV in a calendar year, according to documents on Ninepoint’s website.

The firm is not winding down these funds… “Investors will continue to have access to the ongoing benefits of being invested in private credit as we remain focused on ensuring the sustained performance and stability of our current portfolio.”

Starwood has also gated funds. CEO Sternlicht last week wrote to investors in Starwood REIT that the firm would begin limiting redemptions, and Blackstone’s REIT has already done the same.

“Starwood founder Sternlicht said the change [gating redemptions] at the $9.9 B REIT, the second largest of its kind behind BREIT, is temporary. It is likely to be in place for 6 to 12 months ‘in anticipation of a lower interest rate environment and improved real estate capital market’…During the period of the amended share repurchase, he added, the adviser would waive the 20 pct management fee.

A BBG article cites a recent paper with this headline:

‘Big Banks’ CRE Exposure Rises 40% When REIT Debt is Factored In’ From the piece,

“Collateral damage to the largest banks from intensive credit line draw-downs means that systemic risk from total CRE exposure is probably much greater than if you only look at direct exposure,” said Manasa Gopal, an assistant professor of finance at Georgia Tech, who’s one of the report’s authors.

Ding. Ding. Ding.

The question of course, is whether these problems are systemic. Even if there’s conviction that they could be, the 2007 experience clearly illustrates that timing is important. Additionally, the retail public is conditioned by the financial news networks into the belief that Fed easing will solve, well, everything. What if the Fed’s already behind the curve and is steadfastly holding rates because it doesn’t want to appear political?

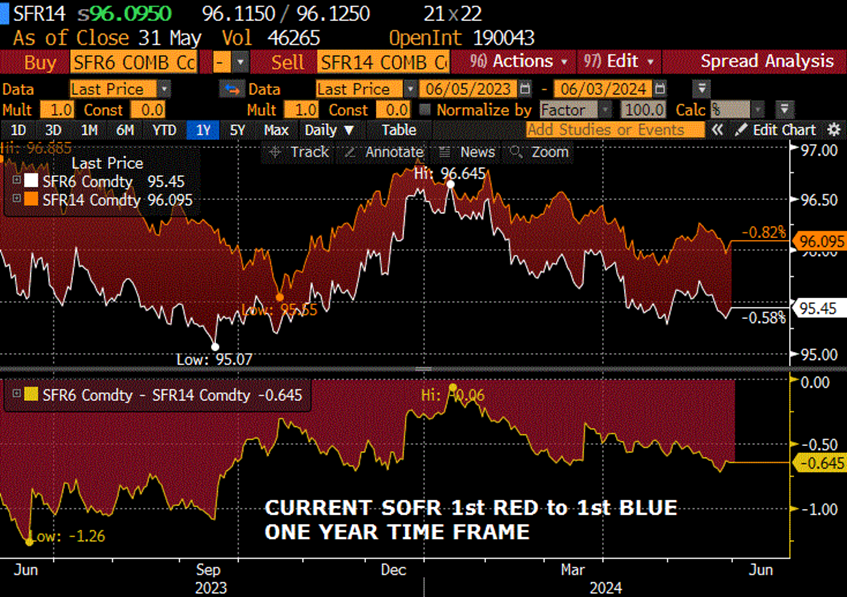

Below I post a couple of Eurodollar calendar spreads relating to the start of the GFC. Top panels show the contract prices and bottom panels are the constant maturity spreads. The hope is to help identify which spreads to favor, though this is just a cursory look.

The first spread is ED5 to ED13, or the first red contract (5th quarterly) to the first blue (13th quarterly). Note that BBG changed the syntax with SOFR contracts, since the first contract continues to trade past the IMM date. That is, on the ED curve the first would have now been June (a forward period contract) and now SFR1 is considered March’24. So for a proper comparison look at SFR6 to SFR14 currently.

In any case, there are a couple of takeaways. First, the spread was positive throughout 2006 and 2007. Even with FF constant at 5.25% from July 2006 to mid-Sept 2007, the first red was pretty much capped at 9550 and the spread ranged from around 0 to +25. Currently the first red to first blue, SFRM5 to SFRM7 is -64.5 (9545/9609.5). The next spread, SFRU5/U7 is -47 (9563.5/9610.5). In a couple of weeks Sept will be first red to first blue. Secondly, futures contracts bottomed and the spread generally rallied from June/July 2007. So, from +33 at the end of June the constant maturity spread rallied to +177 by March’08. My suspicion is that June 2024 and beyond may end up resembling the playbook following June 2007.

If that were to be the case, then buying the forward SOFR spread would be the correct strategy. That’s especially true given the severe inversion currently in place. However, there are mitigating issues this year, including the inflation fight and the election. So rather than buying SFRM5/M7 one might favor SFRU5/U7 (-47) or SFRZ5/Z7 (-32). I do favor a steepening trade, though there can obviously be quite a bit of volatility with this type of structure, and roll is a headwind. Additionally, in 2008 ED5 traded over 9800, or less than 2% yield. My belief is that the Fed no longer wants to push hard toward the zero bound, so reds may be limited on the upside, well below 9800.

Below is the Euro$ chart, first blue to first gold, or the 13th to 17th contract from 2006 to 2008. Notice that in the year of a constant 5.25% FF rate (until Sept 2007) the spread traded in a pretty small range of +8.5 to +16.5. From the beginning of July 2007 to March 2008 it rallied 50 bps to +63. The first blue/first gold SOFR spread has been in a wider range this year, primarily between -1 and +17. It’s now at the low end of that range at +1.0 (SFRM7 9609.5 and SFRM8 9608.5). SFRU7/U8 is +2 (9610.5/9608.5). I could easily see a rally of 50+ bps in these spreads, relative to risk of about 10 from here.

| 5/24/2024 | 5/31/2024 | chg | ||

| UST 2Y | 494.8 | 489.1 | -5.7 | |

| UST 5Y | 452.9 | 452.6 | -0.3 | |

| UST 10Y | 446.6 | 451.2 | 4.6 | |

| UST 30Y | 457.1 | 465.2 | 8.1 | |

| GERM 2Y | 308.7 | 309.7 | 1.0 | |

| GERM 10Y | 258.3 | 266.4 | 8.1 | |

| JPN 20Y | 185.6 | 187.2 | 1.6 | |

| CHINA 10Y | 231.4 | 231.9 | 0.5 | |

| SOFR M4/M5 | -74.3 | -78.5 | -4.3 | |

| SOFR M5/M6 | -54.5 | -52.0 | 2.5 | |

| SOFR M6/M7 | -17.5 | -12.5 | 5.0 | |

| EUR | 108.56 | 108.48 | -0.08 | |

| CRUDE (CLN4) | 77.72 | 76.99 | -0.73 | |

| SPX | 5304.72 | 5277.51 | -27.21 | -0.5% |

| VIX | 11.93 | 12.92 | 0.99 | |

https://www.investopedia.com/articles/07/bear-stearns-collapse.asp

https://www.fdic.gov/analysis/cfr/bank-research-conference/annual-8th/turnbull-jarrow.pdf

https://blinks.bloomberg.com/news/stories/SE92EAT1UM0W

https://www.pionline.com/alternatives/canadas-ninepoint-partners-halts-cash-payouts-3-credit-funds

https://www.perenews.com/starwood-private-reit-gating-will-lead-others-to-consider-it

https://blinks.bloomberg.com/news/stories/SEAXI6T1UM0W