Super Highways

January 5, 2025 – Weekly Comment

*************************************

First, a couple of Fed snippets which highlight a shift back to favoring the inflation mandate (as if the increased inflation dots in the last SEP were too subtle of a hint):

From Tom Barkin’s Fed speech on Friday, Jan 3:

- My baseline outlook is good. How economic policy uncertainty resolves will matter. But, with what we know today, I expect more upside than downside in terms of growth. I see more risk on the inflation side.

Basically, consumer strong but pickier. Jobs balanced, not as much firing and not as much hiring. Productivity gains.

… in my district [Richmond], there’s particular concern about the path forward for the federal workforce.

Second:

From a conference Saturday, both Kugler & Daly “stress inflation fight has not yet been won” (BBG)

****************

Kevin Muir, The MacroTourist, wrote in his latest post that some funds are changing their benchmarks rather than being shackled to performance (and portfolio percentages) of Mag7.

Behind the scenes, many compliance departments and other soberly inclined portfolio managers are questioning the wisdom of being benchmarked to an index that is so exposed to a single group of stocks. Many are choosing to change to a more diversified index.

https://themacrotourist.com/

The implication, depending on how large of a trend this becomes, is that less new money will be funneled into Mag7 and more into the broader market. Currently Mag7 is around 36% of SPX, vs 27% in 2020. (mkt cap Mag7: AAPL, AMZN, GOOGL, META, MSFT, NVDA, TSLA is $17.9T). Some might argue that compliance departments are also becoming heavily “overweight” with respect to the financial industry…

This is from a recent BBG story:

“The world’s 500 richest people got vastly richer in 2024, with Elon Musk, Mark Zuckerberg and Jensen Huang leading the group of billionaires to a new milestone: A combined $10 trillion net worth. [I calculated those three at ~$760 billion]

As a comparison, St Louis Fed has GDP as of Q3 at $29.4T.

What follows is sort of a planes, trains and automobiles comparison vs the information highway. DJT, no, not Donald J Trump but rather the Dow Jones Transports, surged on the election of DJT. From 16252 on Oct 31 to 17618 on Nov 29, a jump of 8.4%. However, as of Dec 31 it was all gone. In fact, on 12/29/23 DJT was 15899. On 12/31/24 it was 15896. No gain over the past year. Nada.

On 12/29/23 META was 354. On 12/31/24 it was 585, a gain of 65%. The market cap rose from about $925b to 1.528T, a rise of $603 billion. The market cap of all companies in DJT is $768b. Those 20 companies combined are worth half as much as Meta. According to slightly dated data on BBG, the DJT companies employ about 1.65 million people. META has 72k employees.

Now, here’s a snippet from Scott Galloway’s 2025 Predictions:

| The AI Company of 2025: Meta |

| No business is better positioned to register progress in AI than Meta. Nine out of 10 internet users (excluding China) are active on Meta platforms. The company has access to more unique human language data, i.e. raw training data, than Google Search, Reddit, Wikipedia, and X combined. In terms of compute, Meta has purchased more Nvidia Hopper GPUs (advanced AI hardware) than any U.S. company other than Microsoft, giving it unmatched AI training and deployment capacity. |

So, looking at things through the lens of Galloway, a technology expert, it’s about AI and tech stocks compared to each other, not to the broader market. Ignoring the stardust of AI, an X post by Daniel T Niles regarding META says in 2025, there is no election and no Olympics to provide a growth boost.

CONFLICT CONFESSION: I am personally short META calls vs long other tech company calls. Very small position.

The point is that 2025 may be the year of rebalancing. Out of tech and into ‘old economy’. Out of growth spurred by Federal Gov’t Deficits and into the private sector. Out of guns into butter. I have no idea whether the net shift will be up or down with respect to US equity markets, but at the margin, the Fed’s re-balance toward inflation rather than employment probably favors the latter.

OTHER TRADE THOUGHTS

My opinion is that the Fed’s 50 bp ease in September was partially sparked by volatility related to yen-carry on August 5. JPY is close to its level of early July just above 161, currently at 157.26. Low on Aug 5 was 141.70. Ten-yr JGB is near last year’s high, set in July, of 1.094% (current 1.085). Japan CPI is 2.9%. BOJ needs to hike. (another rebalance?)

FV to US vol ratio is near DV01 ratio. Last time I recall this happening was when inflation was picking up but the Fed was holding pat, i.e. the long end was leading both in terms of higher yield and higher relative vol. This time it’s more of a deficit scare. (DV01 ratio $124.70 USH v $42.00 FVH or 2.97. Vol ratio 11.85 to 4.14 or 2.86. Usually the vol ratio is more like 75% of DV01 ratio).

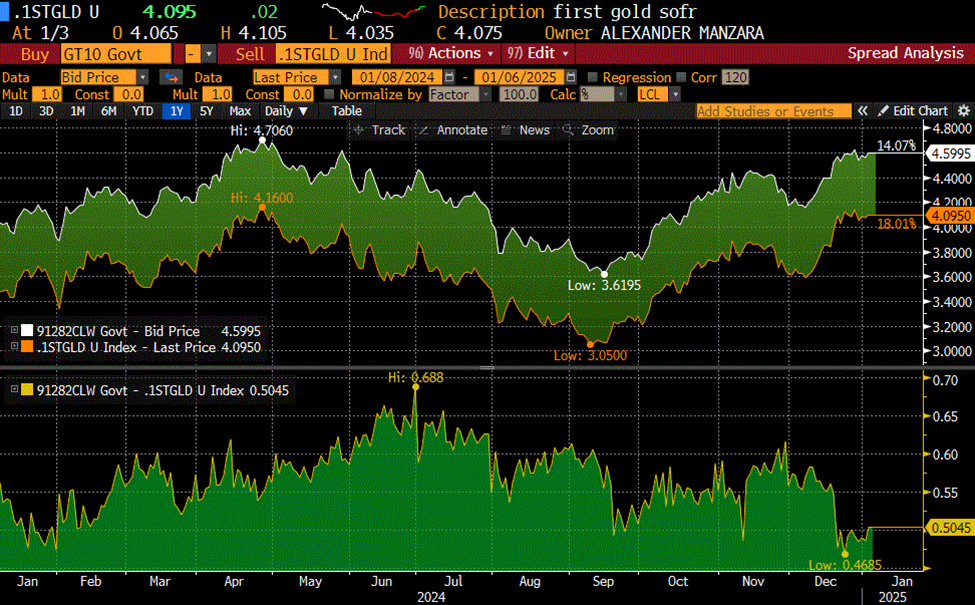

Gold SOFR contracts (5th year forward) appear too high in price (low in yield) relative to treasuries. My opinion is that the red/gold pack spread in SOFR is lagging 2/10 treasury spread. From mid-August to Sept 25, rolling red/gold SOFR spread rallied from 7 bps to 40.75 (up 33.75). Over the same period 2/10 rallied from -20 to +22, 42 bps. Since Nov 25, 2/10 from 0 to +31.5 (new high). Red/gold from -9 to +15 or up 24. Below is first gold to 10y yield, now at a spread of 50bps (nr lows).

Perhaps it’s the adjustment of reds lower (in price) without a corresponding move higher in the 2y yield. For example, on September 11, the yield on SFRH6 vs 2y was 84.5 bps (2s were 3.64% and SFRH6 was 9720.5 or 2.795%). SFRZ5 was essentially the same as SFRH6 so roll doesn’t account for more than a couple of bps. Currently 2s are 4.28% and SFRH6 is 9602.5 or 3.975%, a spread of 30.5 bps.

************************

Auctions of 3s, 10s and 30s ($58b, 39b and 22b) are Monday, Tuesday, Wednesday, moved forward due to the Day of Mourning for President Carter on Thursday. JOLTS on Tuesday. FOMC minutes Wednesday. Payrolls on Friday expected 160k, with Rate unch’d at 4.2%

Other upcoming events:

From the BLS:

Benchmark Release Date

The Bureau of Labor Statistics (BLS) will publish the annual benchmark revision to establishment survey employment data with the February 7, 2025 release of the January 2025 Employment Situation.

https://www.bls.gov/ces/publications/news-release-schedule.htm#:~:text=Benchmark%20Release%20Date,the%20January%202025%20Employment%20Situation.

From Yellen’s recent December 27, 2024 letter to Congress:

Treasury currently expects to reach the new limit between January 14 and January 23, at which time it will be necessary for Treasury to start taking extraordinary measures.

| 12/27/2024 | 1/3/2025 | chg | ||

| UST 2Y | 432.4 | 427.9 | -4.5 | |

| UST 5Y | 445.6 | 441.2 | -4.4 | |

| UST 10Y | 461.9 | 459.8 | -2.1 | wi 459.9 |

| UST 30Y | 481.0 | 481.5 | 0.5 | wi 481.9 |

| GERM 2Y | 210.0 | 216.1 | 6.1 | |

| GERM 10Y | 239.6 | 242.5 | 2.9 | |

| JPN 20Y | 189.5 | 188.2 | -1.3 | |

| CHINA 10Y | 170.1 | 162.1 | -8.0 | |

| SOFR H5/H6 | -17.5 | -21.5 | -4.0 | |

| SOFR H6/H7 | 4.0 | 3.0 | -1.0 | |

| SOFR H7/H8 | 3.5 | 3.5 | 0.0 | |

| EUR | 104.25 | 103.09 | -1.16 | |

| CRUDE (CLH5) | 70.18 | 73.21 | 3.03 | |

| SPX | 5970.84 | 5942.47 | -28.37 | -0.5% |

| VIX | 15.95 | 16.13 | 0.18 | |

| MOVE | 95.20 | 96.67 | 1.47 | |