Signals

October 23, 2022- Weekly comment

A WSJ article by Nick Timiraos on Friday about the Fed stepping down the size of Fed rate increases symbolized a change in policy as surely as Hu Jintao being publicly shuffled out of China’s Party Congress cemented Xi’s control. Of course, hints were already in place. Powell at the August 26 Jackson Hole Conference said that it would be appropriate to slow down the pace of tightening at some point. Brainard in her October 10 speech noted the Fed was attentive to the risk of adverse shocks [from global tightening]. On Friday SF Fed’s Mary Daly was more direct, saying “I think the time is now to start talking about stepping down.”

Markets responded with large moves which were accentuated by intervention in $/yen by the BOJ. The strong USD has represented a tightening in global financial conditions; the range in DXY Friday engulfed the previous ten day’s ranges with a close at 112.01, near the low of the day. While FFX2 settled 9620.5 just 1.5 bps away from what the final settle should be on a 75 bp hike at the November 2 FOMC (9622.0), FFF3 rose 8 bps in price to 9556.0. If the Fed Effective (EFFR) moves from 308 bps to 383 on Nov 2, then another 50 bp hike on Dec 14 would take it to 433 and 75 to 458. FFF3 at 444 (9556.0) leaves it much closer to the former. The November 2 FOMC, now just one and a half weeks away, will be an important event for Fed communication.

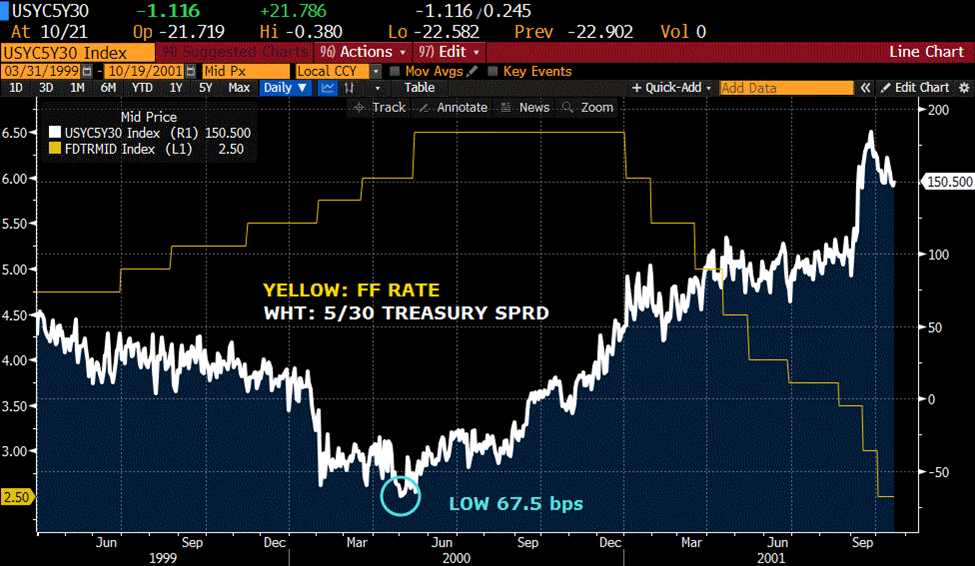

In terms of a specific market-based message on Fed policy, I will focus on the 5/30 treasury spread, and relate that to the death of MMT. Chart of 5/30 below, covering the past two years.

This week the 5/30 spread rallied 28.4 bps to end just above zero. On the chart I have noted recent lows which corresponded to June and September FOMC meetings and CPI releases. The CPI release on June 10 for May was 8.6%. On June 14, 5/30 spread hit the low for the cycle at -17 bps. On June 15, the Fed hiked 75 bps from 0.75-1.0% to 1.5-1.75%, as expected. The ensuing move from June 14 to the end of July took the spread from -17 to +33, or 50 bps in total. Labor market strength and the Fed’s laser message on stopping the scourge on inflation sparked a leg to new lows. CPI on September 13 was 8.3%, the Fed hiked another 75 on Sept 21, and the spread made its ultimate low on Sept 26 at -45.7. Note that last CPI print of 8.2 on October 13 corresponded with a spread price of -28, well above September’s low.

When one views this chart from a longer term perspective, and notes that the lowest price in recent history was -67.5 in May 2000. It’s tempting to say it’s an easy buy, with a stop at new lows. I have fallen into that particular trap many times. Consider red/gold ED pack. Low in 2000 of -8 bps, low towards the end of the hike cycle in 2006, +10.25, low at the end of the hike cycle in 2018, -6. In February of this year, one might have been tempted to pay -10. (how much risk can there be? It’s at ALL TIME lows!). By the end of March it was -72, and extended the low to -87 in April.

Below I isolate the 5/30 spread over the timeframe from April 1999 to October 2001. The low of -67.5 was in May 2000. I have included the FF target rate in yellow. Note that the spread bottomed just prior to the last (outsized 50 bp) hike in mid-May. The spread tends to foreshadow the final tightening by the Fed. Currently, my inclination would be to buy on any dip back towards the June low, with an initial objective to 33, which was the high in late June and is the 38% retrace from the high in Feb of +161 to Sept low -46.

The idea of exiting flatteners and initiating steepeners has been gaining currency. A friend mentioned that MS put out a piece either last week or early this week suggesting that flatteners be exited. If the Fed’s done, curve’s gonna steepen. I believe it’s likely that after December we’re in for a long pause as occurred from June-06 to August-07 at 5.25%. Near term spreads give some credence to that view. SFRZ2/SFRZ3 settled zero. In July it had hit a low of -73. FFF3/FFF4 settled +18. In July the low was negative 69.5. EDZ2/EDZ3 made its low -84 in July, rallied to zero on Sept 26. But is now -23 as turn-of-year concerns are priced into the EDZ2 contract which will still settle to libor.

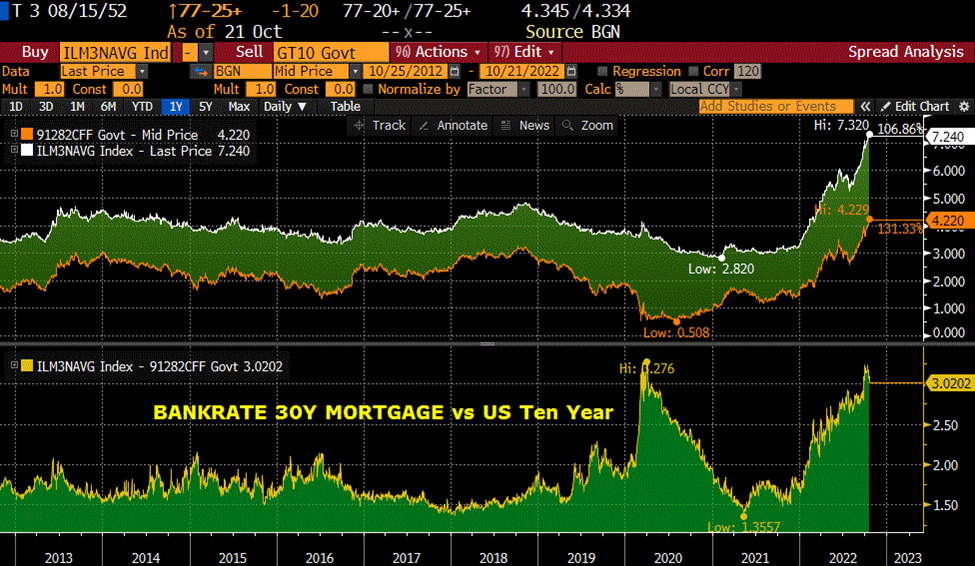

One last bonus chart, the 30yr mortgage to ten year treasury spread nearly reached the Covid high. Another sign of stress that the Fed is surely attentive to.

*********************************

This week (with the resignation of Liz Truss) decisively drove the wooden stake through the heart of Modern Monetary Theory. I am including a link of Stephanie Kelton’s TED talk address ‘The big myth of Government deficits’ which is 13 minutes long and is from August 2021. The message is seductive. Salient clips are at 3:25 and 12:00.

https://www.ted.com/talks/stephanie_kelton_the_big_myth_of_government_deficits?language=en

Around 3:25 “MMT provides an accurate description of how a fiat currency like the US dollar or GBP actually works. It reminds us that we’re no longer on a gold standard, so finding the money to pay for the things we need is never an issue for countries like the US or the UK.”

Around 12 min mark: If resources are already being used…”if the gov’t suddenly tried to make all of these investments at once, it would quickly discover that it doesn’t have the people or the building materials to do the work. To get the resources it needs it would have to compete with the private sector, bidding up wages and prices. THAT would be inflationary and it would be fiscally irresponsible. We are a long way from full employment…”

It’s so godawful stupid in hindsight that it’s almost funny. It’s like saying, “Drive your car just as fast as you want, but if you reach a sharp curve and can’t make the turn and plunge through the guardrail into the ravine, well, then you know you’ve gone too far.” Stephanie Kelton, prophetically referring to the UK in this talk and others, both described and destroyed the concept of MMT in this short speech. No foresight whatsoever. The 5/30 spread and other market signals transparently reflect forward looking concerns (though not always correctly). In 1840 Frederic Bastiat wrote:

In the economic sphere, an act, a habit, an institution, a law produces not only one effect, but a series of effects. Of these effects, the first alone is immediate; it appears simultaneously with its cause; it is seen. The other effects emerge only subsequently; they are not seen. There is only one difference between a good economist and a bad one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those which must be foreseen.

We try to examine past activity and determine what the knock-on effects might be. The lack of foresight inherent in MMT contrasts exactly with current Fed struggles, e.g. not ‘overtightening’ in an environment that is extremely hard to forecast.

This week features Employment Cost Index expected 1.2% for Q3 and Core PCE Prices, expected 5.2% yoy vs 4.9 last. Treasury auctions of $42b 2y, $43b 5y and $35b 7y start Tuesday. There will likely be some concession in treasury futures prices in the early part of the week, though I expect Friday’s lows to hold in FVZ2 (105-1475).

| 10/14/2022 | 10/21/2022 | chg | ||

| UST 2Y | 450.1 | 447.2 | -2.9 | |

| UST 5Y | 426.2 | 434.1 | 7.9 | |

| UST 10Y | 400.2 | 421.7 | 21.5 | |

| UST 30Y | 397.2 | 433.5 | 36.3 | |

| GERM 2Y | 195.6 | 204.1 | 8.5 | |

| GERM 10Y | 234.6 | 241.7 | 7.1 | |

| JPN 30Y | 146.0 | 159.5 | 13.5 | |

| CHINA 10Y | 270.2 | 274.0 | 3.8 | |

| SOFR Z2/Z3 | -6.5 | 0.0 | 6.5 | |

| SOFR Z3/Z4 | -74.5 | -64.5 | 10.0 | |

| SOFR Z4/Z5 | -25.5 | -18.5 | 7.0 | |

| EUR | 97.22 | 98.64 | 1.42 | |

| CRUDE (CLZ2) | 84.65 | 85.05 | 0.40 | |

| SPX | 3583.07 | 3752.75 | 169.68 | 4.7% |

| VIX | 32.02 | 29.69 | -2.33 | |