Merry New Year

December 29, 2024

*********************

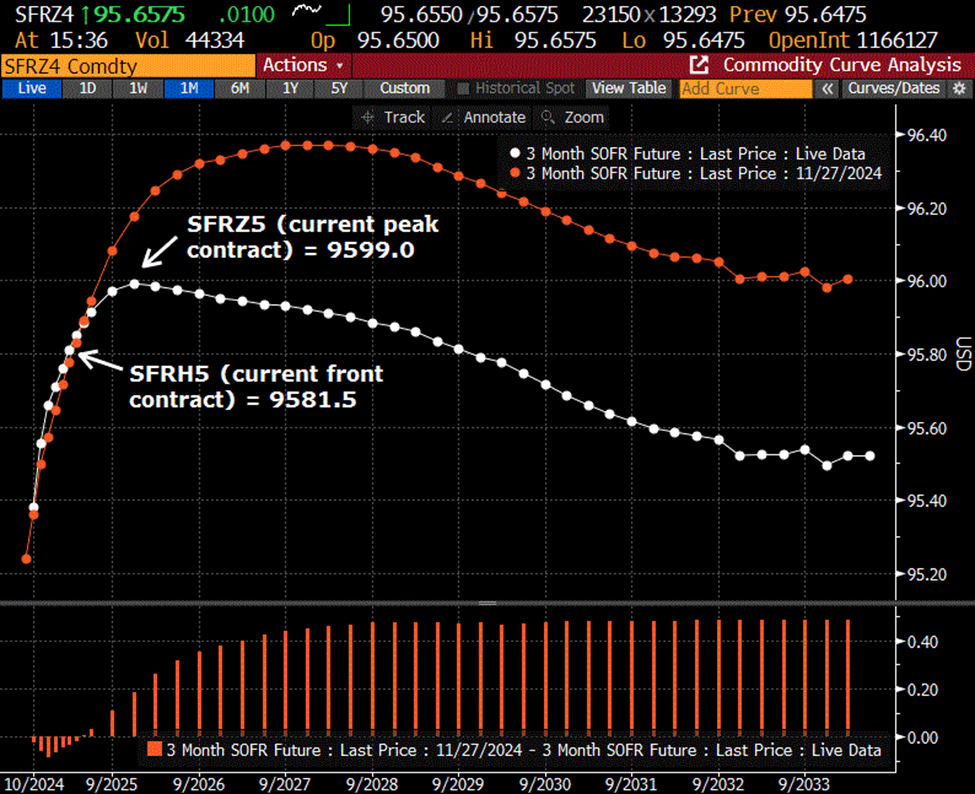

Chart below is the SOFR futures curve. The white dots are from late Friday. The red dots are from one month ago. The obvious change is the shift to lower prices (higher yields). On November 27, the peak contract was SFRU7 at 9637. On Friday SFRU7 settled 9593. The high of this contract on Sept 10 was 9709. As we all know, there’s been a wrenching sell-off in rate futures since the September 18 FOMC.

There are a few other things to notice. First, not a single SOFR contract now is above 9600. That is, all forward rates are above 4%. Secondly, and perhaps more subtle, is that the peak contract on the strip has moved forward in time as back contracts have shifted lower with the steepening curve. The peak contracts as of Friday’s settle were SFRZ5 and SFRH6 at 9599. That means that every calendar spread from March’26 forward is now positive.

I’ve marked the current lowest quarterly contract, SFRH5 at 9581.5 and the peak at 9599, a spread of just -17.5 over a shortened timeframe of just nine months. The implication, if the trend continues, is reduced liquidity going forward. Higher forward rates, stronger USD, cracks in equities… the last signal will be widening credit spreads.

Before the Sept 18 FOMC, the 2nd to 6th one-year SOFR calendar was -130 bps. Of course, since then we’ve had 100 bps of ease, so perhaps the SFRM5/M6 spread at -5.5 (9592/9597.5) makes sense; the front easing has substantially occurred. The issue, as I have repeated, is that asset prices are dependent on lower forward rates discounting future cash flows.

In corroboration with the steepening SOFR curve, 2/10 made a new high for the year of 29.5 bps (4.324%/ 4.619%). The high in 2021 was 158 bps. The low on March 8, 2023 was -108.7. The halfway point is 24 bps which has now been breached. The 0.618 retrace is 55 bps, which is likely the next target. It’s worth noting that while cash tens did NOT make a new high for the year (the April high was 4.706%), thirties did, taking out April’s 4.813% by a bp or so (marked at 4.82 on BBG).

OTHER THOUGHTS/ TRADES

As stocks slid Friday from a ridiculous early week surge, there was a new buyer of 50k SFRM5 9612.5/9662.5cs vs 9556.25p for 3.0 to 3.5 covered 9592. 9612.5c 13.0s OI +43.5k. 9662.5c 6.0s OI +54k. M5 9556.25p 4.0s, OI +42k. Spread settle 3.0 ref 9592.0 settle.

June SOFR options expire 13-June. The FOMC is the 18th. Meetings prior to June are 29-Jan, 19-March, 7-May.

Happy New Year to all! With inflation threatening again, may we all enjoy good health and the prosperity to afford the little luxuries

| 12/20/2024 | 12/27/2024 | chg | ||

| UST 2Y | 431.4 | 432.4 | 1.0 | |

| UST 5Y | 438.0 | 445.6 | 7.6 | |

| UST 10Y | 452.6 | 461.9 | 9.3 | |

| UST 30Y | 471.8 | 481.0 | 9.2 | |

| GERM 2Y | 202.7 | 210.0 | 7.3 | |

| GERM 10Y | 228.5 | 239.6 | 11.1 | |

| JPN 20Y | 185.5 | 189.5 | 4.0 | |

| CHINA 10Y | 171.8 | 170.1 | -1.7 | |

| SOFR H5/H6 | -20.5 | -17.5 | 3.0 | |

| SOFR H6/H7 | -1.0 | 4.0 | 5.0 | |

| SOFR H7/H8 | 1.0 | 3.5 | 2.5 | |

| EUR | 104.30 | 104.25 | -0.05 | |

| CRUDE (CLG5) | 69.46 | 70.60 | 1.14 | |

| SPX | 5930.85 | 5970.84 | 39.99 | 0.7% |

| VIX | 18.36 | 15.95 | -2.41 | |

| MOVE | 90.41 | 95.20 | 4.79 | |

Tech spending race

December 28, 2024

*********************

Just one of those charts from the dotcom bubble. There are a lot like this. This one went from 10 in late 1998 to 110 in Q3 2000. And then, poof.

The fortunes being spent today on data centers for AI are jaw-dropping, but tech leaders are actually worrying about spending too little. ‘When you go through a curve like this, the risk of underinvesting is dramatically greater than the risk of overinvesting for us here,’ Google CEO Sundar Pichai told analysts… Tech CEOs view their investments in data centers as all-purpose bets on the future. If the AI bubble pops, a data center can easily be put to work fueling whatever the next big wave in tech turns out to be.”

I clipped the above from Credit Bubble Bulletin, but the source Axios piece is linked at bottom. The Axios piece has a chart which shows aggregate Capex spending for MSFT, META, GOOGL and AMZN having gone from around $70b in 2019 to $218b in 2024.

When I read the Sundar Pichai quote, it immediately made me think of the dotcom bubble and fiber optic cable. Fiber optic was the backbone of the internet, and the lead company was Corning (GLW), stock pictured above. Of course, to check my memory, I searched for ‘Corning optic fiber’ and was rewarded with this spectacular piece by Kevin Maney from March of this year.

https://kevinmaney.substack.com/p/is-nvidia-remaking-the-movie-corning

He compares Corning with NVDA. It’s not the direct comparison to NVDA which I find interesting, it’s the general theme of a spending race brought on by transformational technology. The winners likely know there will be a shakeout at some point, but they will be left standing (in the rubble).

From the article: “For a while, the strategy looked brilliant. Demand from the Enrons and WorldComs and Level 3s went crazy. They had blank checks from investors to spend, and so they did.”…then…” What once looked like precious and scarce fiber optic bandwidth turned into a glut.”

The promise of AI is efficiency, and the replacement of many professional jobs. Like many transformations, there will be winners and losers.

Here’s a clip quoting Wendell Weeks, who was at the core of Corning’s fiber optic strategy and is now CEO (emphasis added).

“Wall Street had given (these telecom companies) around over half a trillion dollars, and so when people show up with hundreds of millions of dollars to buy your product, you tend to believe them,” Wendell said. “Our big lesson learned was, for one, it’s not enough just to be the best at what you do. You also have to understand your customers’ business model and your customers’ customers’ business model. We were risking more than money. We were risking significant dislocation of people’s lives.

The problem is that dislocations can’t be avoided. Perhaps in recent history they’ve been pushed a bit further forward. The volatility in stocks post-FOMC is a reminder to manage downside risks.

There’s a sobering line in the Big Short by Ben Rickert, in response to Charlie and Jamie celebrating their bet against CMO’s.

“If we’re right, people lose homes. People lose jobs. People lose retirement savings, people lose pensions. You know what I hate about f-cking banking? It reduces people to numbers. Here’s a number – every 1% unemployment goes up, 40,000 people die, did you know that?”

The great part about the Corning (and American) story is this: the company didn’t go out of business. It continued to innovate. Weeks: “We’re never about the products that we make because the products we make will always change. What won’t change is the core of the company being about values and innovation. …We took the opportunity to decide what type of company we were going to be for the next decade. A lot of companies, when they get in that spot, change fundamentally what they are. We instead really embraced the core of what we do, which is to create and make keystone components and to grow through innovation, and acknowledge at the same time there are inevitable downsides.”

The AI boom has created a lot of tech investment geniuses. The other part to remember is that at least part of the background is supported by liquidity. The last FOMC casts shade on the probability of unlimited liquidity.

https://www.axios.com/2024/12/20/big-tech-capex-ai

Bonds wobbly

December 27, 2024

*********************

–In the last two sessions, Tuesday and Thursday, USH5 contract made new lows (113-06 and 113-03) but then closed near the highs of the day (113-28, 113-30). Yesterday was an outside day with a higher close. This price action suggests that selling pressure is becoming exhausted, HOWEVER, this morning’s low is 113-08 and the cash bond yield is again over 4.80, testing the year’s high of 4.813 set in April. A close below 113 would suggest a test of 5%. The high yield in 2023 was 5.115%. The front bond contract at that time reached 107-27. On the opposite end of the world China’s 10y continues to make new low YIELD at 1.70.

–TYH5 settle 108-20. Jan treasury options expire today. Late mkt in Jan 108.5/108.75 strangle was 6/8, indicating a quiet Friday, but the contract currently prints at the lower strike. There are 55k open in the Jan 108.5p strike and 45k in the 108.25p. Not really enough to cause panic, but in a market with fewer participants, maybe an opportunity for a washout. On the call side, just 26k 108.75c and 43k 109c.

–ABC news has this snippet:

Retail sales climbed 3.8% from Nov. 1 to Dec. 24 compared with the same period last year, Mastercard SpendingPulse data showed. The boost in spending exceeded a Mastercard SpendingPulse estimate of 3.2%, while outperforming last year’s growth of 3.1%. The retail sales data excludes automotive purchases.

“Solid spending during this holiday season underscores the strength we observed from the consumer all year,” Michelle Meyer, chief economist at the Mastercard Economics Institute, told ABC News in a statement.

Not much in excess of inflation, but I suppose it goes in the win column.

Treasury yields press higher

December 24, 2024

*********************

–New low settles in FVH5, TYH5 and USH5. 106-02, 108-15, 113-18. Ten year cash yield up 6.7 bps to 4.593%. 2/10 treasury spread near its high for the year at +25 bps. Nearest one-year SOFR calendar is H5/H6 which is also the lowest, but now only -18 (9579, -2.0/9597 -4.5).

–5yr auction today.

–Japan Finance minister Kato warned against excessive moves in fx, but $/yen is still 157.14. Bruce Lee played Kato in the Green Hornet. If it was that Kato giving the warning we’d be at 150.

–FT headline says ‘Defaults on leverage loans soar to highest in 4 years.’ Not much of a surprise, 4 years ago rates were near zero. Fitch reported this a month ago, and the total amount is small, only $73b through October.

From ion analytics:

Annual loan defaults are soaring, with this year’s rate of 4.7% surpassing 4.5% seen during the economic slowdown in 2020 triggered by the advent of the pandemic. It also marks the highest default rate since the global financial crisis, when defaults peaked at 10.5%.

Happy holidays to all

Does USD steamroll higher?

December 23, 2024

*********************

–Back in September, the difference between the lowest contract on the SOFR strip (SFRU4 at 9505) and the peak (SFRM6 at 9721) was -216. Currently, the lowest contract is SFRH5 at 9581 and the peak is SFRU6 at 9603. (I use old euro$ convention and consider H5 as front contract). That spread is -22. Obviously a LOT of easing expectation has been squeezed out of forwards as 100 bps have been cut from Fed Funds. Torsten Slok of Apollo said post-FOMC that he believes there’s a 40% chance of a hike this upcoming year.

–Attached is a chart of India Rupee (new low today vs USD at 85.11), Turkey Lira and Brazil Real. Back in 1997/98 there was the Asian currency crisis. DXY hit its highest level of the year last week, printing just above 108.50. China Renminbi is also at a new low for 2024 at 7.299.

–Today’s news includes Chgo Fed National Activity, expected -0.15 from -0.40, Durables, New Home Sales, Consumer Confidence. 2y auction. Current wi is 4.32%, exactly in line with Fed Effective at 4.33% and SOFRRATE at 4.30.

–Friday featured lower than expected PCE prices, with yoy 2.4% vs 2.5 exp and Core 2.8 vs 2.9. Yields ended lower with tens down 4 bps to 4.526% and back month sofr contracts (greens and blues) +5.0 to +6.5.

Projecting

Weekly comment – December 22, 2024

*****************************************

As mentioned in Friday’s note, I think Q4 2024 has marked a huge turning point. My focus is on liquidity and a tightening in financial conditions, punctuated by the dramatic rise in yields since the Fed’s initial 50 bp FF cut in September. The 30-yr yield has gone from 3.93% on Sept 16 to 4.73% Friday, a rise of 80 bps. Of course, from last December 2024 to the high in April, almost the exact same yield jump occurred, from 3.95% to 4.81%, a slightly larger surge of 86 bps. But that move wasn’t accompanied by an aggregate cut of 100 bps in Fed Funds. DXY also powered higher in Q4, from nearly 100 in late Sept to a new high for the year 108.40 on Thursday. Even the vaunted equity market reacted to the Fed’s admission that inflation is more stubborn than originally thought, with NDX taking a 4.5% tumble after last week’s FOMC. On the other hand, when the 30y hit 4.81% in April, NDX eased to 17000; it’s now 25% higher at 21290.

Political tumult has made market moves seem relatively tame, with Trump’s election sparking government collapse throughout the world. Up next, Trudeau. Amazingly, gold has had a muted response, from 2580 on 9/16 to 2620 Friday. It’s a different story for Bitcoin, from 60k to 100k.

The most important event last week was the Fed’s tacit swing back to inflation as the most important mandate. Projections for PCE inflation jumped from September to December, while the UE rate projection was trimmed. My guess is that the pendulum will swing back to employment as the No. 1 concern, probably by mid-year. Financial Stability might also press its case for official mandate status.

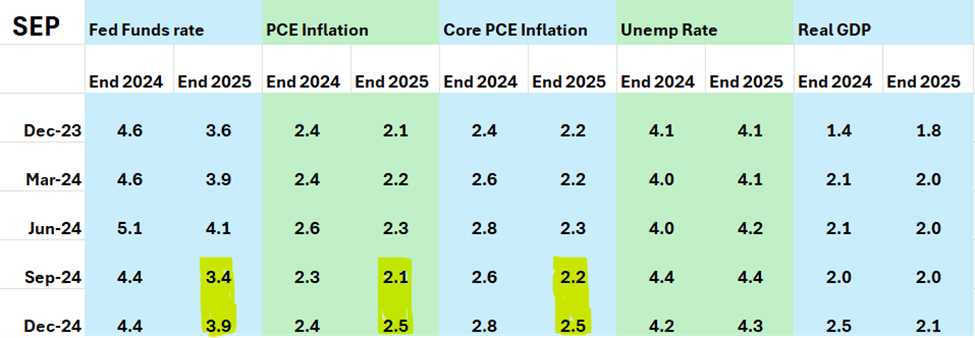

The table below is created from the Fed’s Summary of Economic Projections. There are a few things to notice, but the most glaring are highlighted in yellow: changes for end-of-2025 forecasts regarding Fed Funds and inflation. FF’s are up 50 bps from the September projection (3.4% to 3.9%) and inflation measures are up 3 to 4 tenths, with both headline and core now projected at 2.5%.

Moving from left to right, in the FF columns, the Fed had pretty much penciled in a cut of 100 bps in 2025, except for March which only had a 75 bp projection. For example in Sept, the Fed estimated 4.4% for the end of 2024 (correct) but 3.4% for end of 2025. However, it’s now just 50! (4.3 to 3.9). End-of-2025 inflation guesses were steady until last week’s jump which now forecasts a significant delay in reaching the goal of 2% inflation. The unemployment rate and GDP are relatively stable for 2025, but UE went down 1 tenth and GDP up 1 tenth in the last SEP. In my opinion, that’s a nod to the idea that the new administration is going to try to run things just a little bit hot.

The other thing perhaps worth mention regards the ‘neutral rate’. If the unemployment rate and real GDP are relatively stable, (as is the case in 2025 projections) then I think it’s fair to say that FF minus PCE inflation is the neutral rate. In Dec of last year 1.5, in March 1.7, in June 1.8 in Sept 1.3 and at the last FOMC 1.4. So maybe 1.3 to 1.4 runs things warm and 1.5 to 1.6 is neutral. Fed officials often seem bewildered when asked to identify the neutral rate, but it’s right there in the table. Most recent CPI is 2.7%, with PCE 2.4% and PCE Core 2.8%. FF effective is 4.33%. SOFR is 4.30%. So we’re currently 4.3 – 2.6 or 1.7%. It can be argued that we’re at neutral NOW.

On September 10, SFRZ5 settled at the high of the year 9720. On Friday it settled 9599.5, a jump in yield of 120 bps. The current level is only 30 bps below SOFRRATE. It’s more-or-less in line with the Fed’s most recent projection of 3.9% for end-of-year FFs. Is it “right”? To be determined. I would also note that on Friday, every SOFR contract from December 2025 to December 2028 settled between 9599.5 and 9603, right around 4%. As I wrote Friday, in September the reds (second year forward) were all around 2.8- 2.9% in yield. If you think that a higher discount rate applied to forward earnings is a negative headwind for asset prices, then it’s right to exhibit a modicum of caution. If you think that deregulation, lower taxes, and on-shoring of US manufacturing is a gale-force tailwind that will overwhelm a few bps of higher rates, then just stick with the advice that every ‘wealth manager’ repeats (as if recent history has increased their respective IQs by the same percentage as AI stock gains): Buy more.

OTHER THOUGHTS/ TRADES

The new Fed Effective rate of 4.33% is below every treasury yield except the 2y which ended Friday 4.314%. It’s 20 bps below tens (4.526%).

FFF5/FFG5 settled -2.0 (9567.5/9569.5). The next FOMC is Jan 29, so if the Fed were to ease at that time, FFG5 would go to 9592 or 4.08% Fed Effective. Clearly, the market is anticipating a ‘skip’. What is somewhat surprising is FFG5/FFJ5 spread at -12 (9569.5/9581.5). Both Feb and April are ‘clean’ months, i.e. no Fed meetings. March FOMC is 3/19. As of now, the market is pricing near 50/50 odds of an ease in March. I would think that spread would be more appropriately priced around -7. Also, at 9569.5 FFG5 has 2.5 bps of likely risk. January covers the inauguration and the FOMC meeting. Ukraine just rammed drones into a high-rise building in Kazan. A missile from Yemen penetrated Tel Aviv. The US has unexplained drones buzzing around cities and military installations. Is long FFG5 a worthwhile insurance policy? Not sure, but I’ve seen (and done) worse things.

A couple of weeks ago I recommended buying USF 118/116.5/115 p fly for 10/64s. At the time USH5 was 120-05. My thought was that USH5 could retrace lower, to around the middle strike of the fly. Good example of the right idea with the wrong vehicle. The market sold off so quickly that the fly settled Friday at 16, with USH5 now under the bottom strike at 114-16. Expiration is Friday. I had also suggested buying TYH 108/115 strangle for 30 as I thought treasury vol was underpriced. On Friday the strangle settled 50 ref 108-195. Needs to be delta hedged or exited.

Regarding SFRZ5, on Nov 14 there was a seller of about 50k Z5 9600p at 37 ref 9614.5. There’s nothing tremendously special about this trade; I just mention it due to the 2025 ‘dots’. Just prior to the sale, Z5 9612.5 atm straddle was 90, and it immediately fell to 88.5. By Dec 6, the contract was 9629 and the 9600p was 29.0. On Friday the contract settled 9599.5 and the put 39.0. The atm straddle is now 77.5. According to the current SOFR setting, (equal to 9570) that put short should be safe. Equidistant 9675c and 9525p settled 16.75 and 12.75, so there’s a bit of upside skew, but not nearly as much as there had been a couple of months ago. The question is, can the market possibly start tilting towards the idea of hikes rather than cuts in 2025?

I’m not making projections. Just considering possibilities. I think the range of scenarios for 2025 is enormous. Happy Holidays!!!!!!!

Treasury auctions this week:

MON 2y, $69b

TUES 5y, $70b

THUR 7y $44b

| 12/13/2024 | 12/20/2024 | chg | ||

| UST 2Y | 424.9 | 431.4 | 6.5 | |

| UST 5Y | 425.2 | 438.0 | 12.8 | |

| UST 10Y | 439.9 | 452.6 | 12.7 | |

| UST 30Y | 460.3 | 471.8 | 11.5 | |

| GERM 2Y | 207.1 | 202.7 | -4.4 | |

| GERM 10Y | 225.7 | 228.5 | 2.8 | |

| JPN 20Y | 184.1 | 185.5 | 1.4 | |

| CHINA 10Y | 178.2 | 171.8 | -6.4 | |

| SOFR H5/H6 | -30.0 | -20.5 | 9.5 | |

| SOFR H6/H7 | -3.0 | -1.0 | 2.0 | |

| SOFR H7/H8 | -0.5 | 1.0 | 1.5 | |

| EUR | 105.01 | 104.30 | -0.71 | |

| CRUDE (CLG5) | 70.82 | 69.46 | -1.36 | |

| SPX | 6051.09 | 5930.85 | -120.24 | -2.0% |

| VIX | 13.81 | 18.36 | 4.55 | |

| MOVE | 85.66 | 90.41 | 4.75 | |

This material is not a research report prepared by R.J. O’Brien & Associates LLC. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions. You must be in possession of a functioning brain.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. Copyright 2024. Alex Manzara

In: Eurodollar Options

Trend in financial conditions has reversed

December 20, 2024

*********************

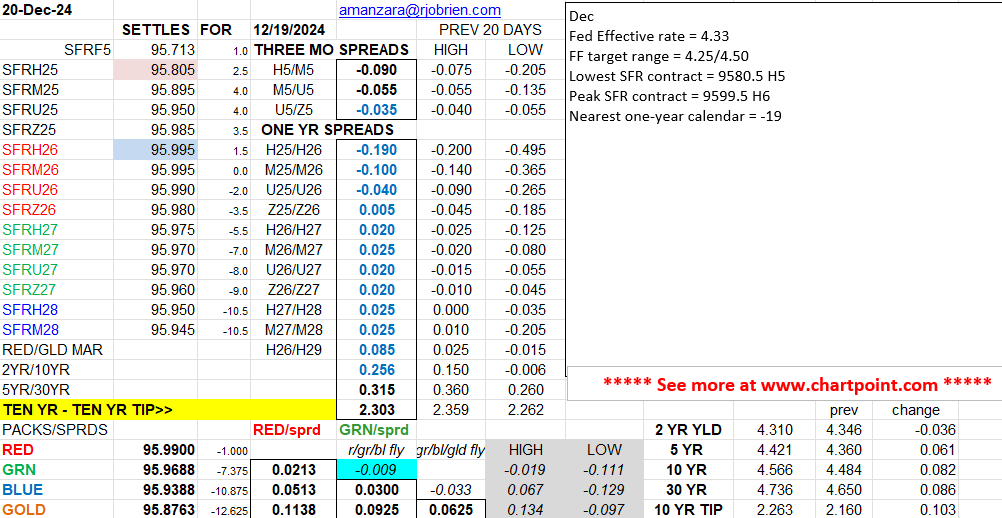

–Usually I jot down a few notes about changes in SOFR spreads, or maybe an interesting macro tidbit. But current market moves appear to me to be a complete change in market dynamics, with signals of a harsh reversal in liquidity and financial conditions. Instead of BTFD it’s now STFR (sell rallies). I might be incorrect, but whether you think it was Powell that created the change or the bond vigilantes, or the market in general, I am marking Q4 2024 as a sea change, starting with the Sept 18 FOMC.

–As mentioned before, Dudley, former president of the NY Fed listed financial conditions as short and long term rates, the value of the dollar, equities and credit spreads. The 30y bond yield ended at 4.736 (ref USH5 settle 114-01). It’s nearing the high of the year set April 25, 4.813%. Tens ended 4.566%, the April high was 4.706%. The change in the SOFR strip has been dramatic. Just before the Sept FOMC, the reds were above 9700, as high as 9720. That is, forward rates were 3% or a bit lower. Those forward levels provided a pillar of support for equity valuations. Yesterday was the first time that all SOFR contracts 5 years out had a 95 handle…now there’s no longer any contract above 9600 (sub-4%). On the attached pdf I note the lowest SOFR contract and the peak. The lowest contract has been the first quarterly, formerly SFRZ4 when it was the lead, and now SFRH5 at 9580.5. The peak contract had been back further in the greens, at least a couple of years away. As of last night it’s SFRH6 at 9599.5. SFRH5/H6 spread settled at a new high -19.0. Equities have been hammered since Powell’s presser. DXY set a new high for the year yesterday at 108.40. Credit spreads have been extremely tight, but take a look at hi-yield ETFs JNK and HYG – cliff dives in the past two days. I’m not saying we can’t get bounces, but the trend in conditions has changed.

–News today includes PCE prices expected m/m 0.2 from 0.2 with Core 0.2 from 0.3. Yoy 2.5 from 2.3 and Core 2.9 from 2.8.

–The new Fed Effective should be 4.33%. That’s a price of 9567.0. Jan FF settled 9567.5 and Feb FF, which prices the Jan 29 FOMC settled 9569.5. So there’s a tiny bit of ease priced, but not much. If the Fed were to cut by another 25 that spread would be valued at -23.4. Headline on FT this morning: ‘China’s short-term bond yields fall back below 1% for the first time since 2009’.

Hawk tuah

December 19, 2024

*********************

–That was what the professionals might call, “a hawkish cut”. A couple of weeks ago I had thought the Fed might hold and BOJ hike. Wrong. Only Beth Hammack, Cleveland Fed President saw it my way, she dissented in favor of holding rates steady. Barely mattered as yields jumped, with weakest SOFR contracts down 15 on the day: SFRZ5 9595, H6 9598 and M6 9599.5 (all down 15). We’ll get back to SFRZ5 in a minute. BOJ held rates steady. Stocks were crushed with Nasdaq Comp -3.6% and SPX -3.0%. Hopes of an accommodative Fed were dashed.

–Changes in the quarterly Summary of Econ Projections (SEP) were startling. Estimates for the end of 2025 from September to yesterday:

Unemployment 4.4% to 4.3% (well that’s going to be wrong)

PCE inflation 2.1% to 2.5%

PCE Core 2.2% to 2.5%

FF projection 3.4% to 3.9% and then 3.9% back down to 3.4% for end-of-2026

–So in September the Fed had penciled in a cut of 100 bps over the coming year, and now it was shaved to just 50. The goal of 2% inflation was pushed back into 2026. Now using SFRH5 as the front contract, the lowest 1-yr calendar is H’25/H’26 which settled -20 (9578, down 5 and 9598, down 15). SFRZ5 at 9595 is a rate of 4.05% fairly close to the new Fed projection of 3.9%. Current Fed Effective EFFR should be 4.33%. It appears from 2025 estimates that the Fed’s notion of neutral is around 1.4% which is perhaps low.

–USH5 contract at a new low this morning 114-18. 30yr yield around 4.71%. $/yen has exploded higher, now 156.86.

Elevator down

December 11, 2024

*********************

–Yields up a few bps yesterday going into today’s CPI. Expectations are 0.3 m/m for both headline and Core. On y/y headline expected 2.7 from 2.6 and Core 3.3 from 3.3. Steady numbers…unless you drink coffee. Front end contracts remain convinced of a Fed ease one week from today. FFZ4 settled 9550.75. A price of 9547.25 would indicate 50/50 odds, but the Fed generally never disappoints market pricing. Ten year auction today as well.

–Ten year yield up 2.2 bps to 4.219%. Reds were weakest on the SOFR strip, down 3.5 (SFRZ5 -3.5 to 9522.5). USH5 contract topped on Sept 17 at 127-24, one day before the Fed’s initial 50 bp cut. Selling commenced. The low on Nov 6, one day before the Fed’s second rate cut of 25 bps, was 115-13, which was touched again on Nov 18, exactly two months after the first ease. Since then there was a bounce up to Friday’s high 119-17, but this week so far has seen selling back under 119. Feels like a “stairs up, elevator down” set-up.

–The value of USD is not under the Fed’s purview, but India’s rupee is making new lows. Larger GDP than the UK and nearly as large as Canada and Mexico combined. A strong USD helps in terms of the Fed’s inflation goals, but the new admin wants a weaker currency to support on-shoring.

Below is coffee chart:

NFIB optimism. Will it bear out?

December 10, 2024

********************

–Yields a touch higher in front of this week’s auctions; 3y today. Ten year re-open tomorrow, ended at 4.197% up 4.8 bps on the day. On the SOFR strip reds through golds down 3 to 4 bps. Notable new buyer of 50k SFRJ5 9625/9700cs for 11.0. Settled 11 ref 9608 in SFRM5.

–Nasdaq Comp slight outside day range after posting a new all-time high. Reversal signal (for short-term at least).

–Today’s news, just released, includes NFIB Small Biz Optimism 93.7 last. Surged to 101.7 in November. Not surprising given election results. From NFIB:

The NFIB Small Business Optimism Index rose by eight points in November to 101.7, after 34 months of remaining below the 50-year average of 98. This is the highest reading since June 2021.

From Chief Economist Dunkelberg

“The election results signal a major shift in economic policy, leading to a surge in optimism among small business owners. Main Street also became more certain about future business conditions following the election, breaking a nearly three-year streak of record high uncertainty. Owners are particularly hopeful for tax and regulation policies that favor strong economic growth as well as relief from inflationary pressures. In addition, small business owners are eager to expand their operations.”

–Tomorrow is the big data point: CPI. SFRZ4 options and Dec midcurves expire Friday. SFRZ4 9562.5 straddle settled 4.5 with futures right at strike. 0QZ4 (red) 9625^ settled 11.5 with SFRZ5 9626.

–RBA held rates steady, but aussie dollar is near the low of the year (0.6397 in expiring Dec future). Hang Seng continues to surge after China’s vows of support for equities, property.

NOTE: This report will cease after tomorrow for a week due to Mandatory Time Off policy.

This material has been prepared by a sales or trading employee or agent of R.J. O’Brien & Associates LLC and is, or is in the nature of, a solicitation. This material is not a research report prepared by R.J. O’Brien & Associates LLC. By accepting this communication, you agree that you are an experienced user of the futures markets, capable of making independent trading decisions, and agree that you are not, and will not, rely solely on this communication in making trading decisions.

DISTRIBUTION IN SOME JURISDICTIONS MAY BE PROHIBITED OR RESTRICTED BY LAW. PERSONS IN POSSESSION OF THIS COMMUNICATION INDIRECTLY SHOULD INFORM THEMSELVES ABOUT AND OBSERVE ANY SUCH PROHIBITION OR RESTRICTIONS. TO THE EXTENT THAT YOU HAVE RECEIVED THIS COMMUNICATION INDIRECTLY AND SOLICITATIONS ARE PROHIBITED IN YOUR JURISDICTION WITHOUT REGISTRATION, THE MARKET COMMENTARY IN THIS COMMUNICATION SHOULD NOT BE CONSIDERED A SOLICITATION.

The risk of loss in trading futures and/or options is substantial and each investor and/or trader must consider whether this is a suitable investment. Past performance, whether actual or indicated by simulated historical tests of strategies, is not indicative of future results. Trading advice is based on information taken from trades and statistical services and other sources that R.J. O’Brien & Associates LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. Copyright 2024. Alex Manzara