Gliding into the end of the week

January 24, 2025

******************

–Quiet Thursday featuring lower vol and a slightly steeper curve. SFRH6 remains the peak SOFR contract at 9602.5 (+2 on the day). H’27 9595.5 (+0.5) and H’28 9588.0 (-1.5). Ten-yr treasury yield rose 3.8 bps to 4.635. The 2y yield fell 1.5 to 4.28%. 2/10 spread 35.5 and up another 1 bp this morning. Trump is, of course, calling for lower rates, but it has been apparent from price action that the Fed lowering the funds rate has translated into higher long-end yields as inflation concerns are rekindled.

–Feb treasury options expire today. Obviously some replacement trades, with a buyer of 32k TYJ5 112c with TYK5 112.5c for 21. The April calls settled 8 with a jump in open interest of 47k and May settled 13 with an OI increase of 33k. Deltas are 9 and 13, so an equivalent futures (using OI changes) add of 8500 longs. TY futures open interest added 11k.

–BOJ hiked by 25 as expected. Ueda ‘sees inflation trend settling at 2% around FY 2026’ Not much change in yen or JGB, the latter at 1.223% up a couple of bps. Pre-yen carry volatility 10y JGB had peaked near 1.1%, then fell back to 80 bp in early August tumult. Since September, the 10y JGB yield has pushed higher, from 80 to 1.25%. Over the same time frame US 10y from 3.75 to 4.75%. And we’re all looking for the holy grail of 2% inflation. (He chose poorly).

–News today includes Global US Composite PMI expected 55.6 from 55.4. Existing Home Sales.

Could Fed Flip?

January 23, 2025

*******************

–Some large option trades in rates in an otherwise unremarkable session. Ten year yield rose 2.3 bps to 4.597%. Stocks soared. with SPX up 0.6% and Nasdaq Comp +1.3% just shy of new all-time highs.

–Early buyer (new) 50k SFRU5 9587.5/9562.5/9537.5p fly for 7.0. Settled there vs 9596.5. For a roll comparison, same put fly in SFRM5 ref 9588.5 is 9.0. And in SFRH5 vs 9575.0, 13.75s.

–Exit seller 60k SFRM5 9612.5/9662.5cs 4.25 to 4.0; future settle 9588.5, with cs settle 3.75 (7.0/3.25).

–New buyer (add) 30k 0QM5 9712.5c 4.5; settled 4.25

–Exit seller 50k 0QH 9550p at 2.5 covered vs 9600.5 down to 9600.

–New seller 0QU 9600^ 5k 73.5 to 73, settled 73.0 ref 9598.0 in SFRU6

–New buyer 50k TYH 102p for 1.

–Recent theme in rates is a shift toward limited or no ease going forward. In SOFR yesterday, flows were mixed, but I’ll focus on selling calls, buying puts, selling vol. Near SOFR straddles eased by a couple of bps. The 0QU straddle was sold at 74 on Tuesday, and then down to 73 yesterday.

–Highest contract on the SOFR strip is H6 at 9600.5. But let’s consider SFRZ5 since it has over 1m in open interest and seems to be a favored vehicle for those that trade on the basis of Fed ‘dots’. Z5 settled 9600 and was at a peak of 9725 on Sept 11, just over 4 months ago. A yield jump of 125 bps since the first ease! The latest Fed projection for year-end 2025 on Fed Funds was 3.9% or a price of 9610. But that projection in September was 3.4%. Could we possibly get a shift in expectations (and dots) to something like 2 HIKES before year-end? Fed Effective is currently 4.33%. Is a return to 4.83% out of the question? That would put SFRZ5 down to 9515-ish. We don’t often see the Fed quickly reverse course once they’ve started a new (easing) cycle. On the other hand, look how quickly the new admin has upended previous policies. It’s day three! In that context, I might be more inclined as a buyer of 0QH 9550p for 2.5 rather than seller. Something like 0QJ 9550/9500ps (SFRM6 underlying) is around 4.0. Not a recommendation, just a thought process.

Flattening Continues

January 22, 2025

******************

–Main feature Tuesday was curve flattening, with heavy selling pressure on 2yr notes. In cash, 2s rose in yield just over 1 bp to 4.281% while 10s fell 3.5 to 4.574%. In futures, TUH5 fell 0.25/32s while TYH5 was +6/32s at 108-23+. Last Thursday a large block trade occurred, selling 52k TUH5 vs buying 23k UXYH5. At the time 2/10 was around 37-38 bps, yesterday I marked the spread at 29.3 at futures settle. It appears that front end sales are longs liquidating. Open interest fell 29k in TU and 20k in FV while rising 43.7k in TY.

–There was a new buyer of 30k 0QM5 9712.5c for 5.0, some outright and some covered 9601; settled 4.75 vs an unchanged future settlement of 9600.5 in SFRM6. While there were a few other upside plays in SOFR, flattening was apparent there as well, with the red pack (2nd year) unch’d, while greens (3rd) were +1.625 and blues (4th) were +3.125. Several analysts are echoing Waller and saying several eases are likely this year, but the futures curve isn’t really embracing that view. SFRH5/H6 one-year calendar settled -25 (9576/96010). FFG5/FFG6 settled -38.5 (9567.5/9606). These spreads are indicative of 1 to 1.5 cuts over the year, with odds of the March 19 FOMC specifically at about 25%. (FFG5/J5 spread is -6). Might be a few eases, might be none. Is a hike out of the question? Nope.

–Dollar index fell hard yesterday and is continuing lower this morning. Last at 107.80; on 1/13 it had peaked above 110. A bit of a tailwind for commodities like corn and gold. which have rallied throughout January.

Listened to an interesting clip by Paulo Macro on X

https://x.com/PauloMacro/status/1881743476578255126

One funny line is that he says the west has created the “turducken” of financial disasters. He cites a generational divide, for which he lays blame squarely at the feet of the boomers. “…boomers are the second largest cohort generation-wise in America at 20% of the population, and never in history have we seen a cohort of that size end up with over half the assets in America, while the Millennials who are bigger at 25% of the population hold 6% of assets . And the income levels between those two groups are wildly disparate…” He goes on to claim that tensions arising from this wealth and income disparity are contributing to lottery-like speculation on crypto, etc.

(around 7:20 mark)

Stressed?

January 21, 2025

******************

–The titans of tech were on display at the inauguration. Musk, Cook, Zuck, PichAI, Bezos. I didn’t watch much, but what I didn’t see were banking and finance giants. I guess they’re in Davos.

–BBG has an editorial today: Fed’s Bank Stress Tests Are Facing a Stress Test.

https://blinks.bloomberg.com/news/stories/SQ8BWKT1UM0W

The article notes that at the four largest US banks, equity capital as a share of total exposure has declined from around 7.2% in 2017 to 6.1% now. A Fed note seeking public comment on Stress Tests from Dec 23, 2024 was cited. (Seems like a lagged response from the BBG editorial staff).

https://www.federalreserve.gov/newsevents/pressreleases/bcreg20241223a.htm

–My thought is that the unwritten Fed mandate of financial stability might get thrust into the limelight. perhaps overwhelming inflation and jobs. Trump embodies volatility, and the Trump coin highlights crypto risks and a gambling mentality. Perhaps of larger concern is the rise of private credit. I did not read the source article, but Almost Daily Grants (ADG) emphasizes comments made to the FT by Nick Moakes (Wellcome Trust CIO):

“if the world gets a little bit more difficult economically, I think there are some accidents waiting to happen in the private credit world. . . [the industry] has sucked in an enormous amount of capital. That has meant that the lending standards that are applied in certain parts of private credit markets have diminished.”

…“You can construct all kinds of cataclysmic scenarios where they take each other down, but actually, they won’t, because what they’ve done is very clever. This stuff is all sitting in LP vehicles. So, the liability is all with the investors.”

–Another ADG article notes: “For context, buyout firms issued $68.3 billion in loans to pay themselves dividends last year, the second-highest total on record behind 2021’s $73.2 billion haul.” This sentence refers to dividend recaps, where buyout firms issue debt in order to extract cash through dividends. The amounts cited aren’t particularly large. But the broader context encompasses all of the potential stress just underneath the TBTF financial behemoths. Bank stress tests are simply a high visibility signaling mechanism. The risks are skimming below the surface.

Musing about the Composition of Employment

January 19, 2025

******************

Last week I touched on the decline in yields which began globally in Q3 2018. In November 2018, tens were 3.24 and fell though 2019 to 1.50 by September. Another huge decline followed as Covid hit in late 2019 into Q1 2020.

I don’t think we will copy that experience, but last week featured a solid performance in bonds, with yields falling smartly, more than reversing the previous week’s rise which was associated with the blowout payrolls report.

In the past week yield declines were as follow: 5s -17.5 to 4.415%, 10s -16.3 to 4.609% and 30s -12 to 4.844%. On the SOFR strip, greens (3rd yr forward, H7, M7, U7, Z7) led the way higher, ending +19. The green pack (avg of 4 contracts) settled 9593.75 or 4.0625%. The main catalyst was lower than expected CPI with m/m Core up 0.2% and yoy 3.2% vs 3.3% expected. With Wednesday’s release of CPI, the previous Friday’s sell-off (sparked by 256k NFP) was erased. Though CPI is nowhere near the Fed’s target, Waller still opined that three to four eases could occur this year.

My first sentence in last week’s note was: “I don’t believe the payroll data.” Last week’s price action concurred. The strong jobs report was dismissed. There have been many explanations for solid economic data and payroll anomalies, many related to the difficulties in capturing illegal immigrants’ influence on various economic data. What’s pretty clear in the short term is that there will be job losses both in gov’t jobs (which were another major growth industry in the past few years) and undocumented workers.

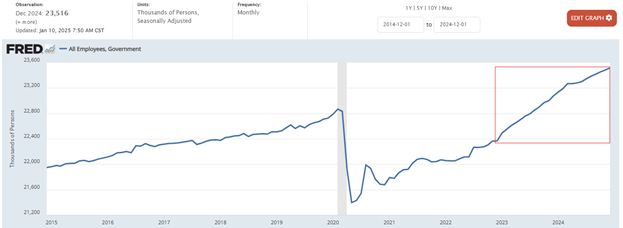

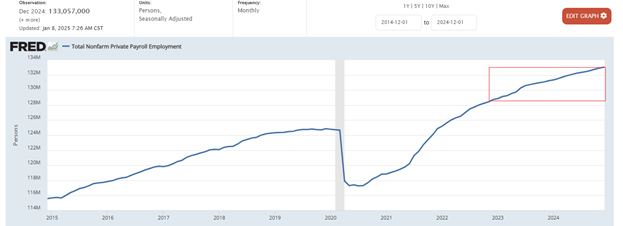

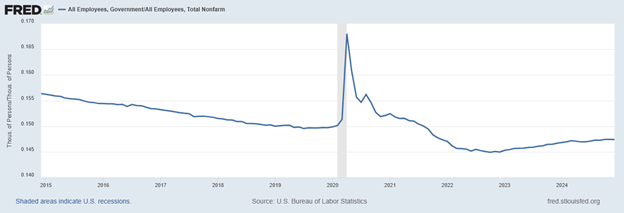

In the last two years, total Gov’t employment went up just over 5.1% from 22.367m in Dec 2022 to 23.516m in Dec 2024. Over the same period, Total Private nonfarm employment rose 3.6% from 128.426m to 133.057m. The charts below indicate relative gains over the past two years in the red rectangles. Top chart is Gov’t Employees (USGOVT on St Louis Fed Fred) and the lower chart is total non-farm Private Payrolls (ADPMNUSNERSA). This is what DOGE is likely to address. However, even if the last two years of gov’t jobs were eliminated, it’s only 1.15m jobs, which is less than 1% of private payrolls. Ignoring other factors, it seems to me that new business incentives could lead to a fairly painless (in aggregate) hand-off from Gov’t to Private employment.

In fact, to be fair, and this is quite surprising to me as I looked at the data, the percentage of Gov’t payrolls to Total Nonfarms has had a pretty modest bounce in the past two years. The ratio chart is below.

We know that government deficits have exploded in the past several years, which has led to investor trepidation with respect to long-bond yields. Since Q3 2022 to Q3 2024 the Federal Debt grew 15.2% from $26.851T to $30.966T or 15.2%. But those gains haven’t sparked the same percentage magnitude in employment. Perhaps the gov’t is ALREADY getting more efficient. We’re spending MORE PER EMPLOYEE! Hahahahahahah, that’s a good one, right? The deficits seem more related to government transfers, to both the US population and to foreign lands.

Treasury Sec’y nominee Scott Bessent repeatedly said at his hearing last week that the US has a spending problem, not a taxation problem. I suspect cuts in spending will happen quite rapidly. An interesting line from John Mauldin’s weekend missive:

I think we can expect the White House to get organized faster than they did in 2017, simply because they have more experience and will get their people in place more quickly. “At President Trump’s inauguration in 2017, he had filled 25 appointments (no typo) of the thousands of open spots required to be filled by the new administration. Going into next week’s inauguration, two thousand positions have been filled.” (h/t David Bahnsen)

A 50% retrace of the 10y yield rise from mid-Sept to last week is 4.21%. (3.62 to 4.79). In futures, 110-24 to 111-08 is a reasonable target for those who believe that a change in gov’t spending trajectory can provide legs to last week’s rally.

| 1/10/2025 | 1/17/2025 | chg | ||

| UST 2Y | 439.2 | 427.0 | -12.2 | |

| UST 5Y | 459.0 | 441.5 | -17.5 | |

| UST 10Y | 477.2 | 460.9 | -16.3 | |

| UST 30Y | 496.3 | 484.4 | -11.9 | |

| GERM 2Y | 228.4 | 222.9 | -5.5 | |

| GERM 10Y | 259.5 | 253.5 | -6.0 | |

| JPN 20Y | 195.9 | 191.0 | -4.9 | |

| CHINA 10Y | 165.3 | 166.1 | 0.8 | |

| SOFR H5/H6 | -12.5 | -24.0 | -11.5 | |

| SOFR H6/H7 | 10.0 | 5.5 | -4.5 | |

| SOFR H7/H8 | 6.5 | 6.5 | 0.0 | |

| EUR | 102.55 | 102.76 | 0.21 | |

| CRUDE (CLH5) | 75.75 | 77.39 | 1.64 | |

| SPX | 5827.04 | 5996.66 | 169.62 | 2.9% |

| VIX | 19.54 | 15.97 | -3.57 | |

| MOVE | 99.73 | 92.72 | -7.01 | |

Something Brewing

January 17, 2025

******************

–There was a large 2/10 flattener printed on block yesterday morning at 9:03ET.

-52k TUH5 102-22.625

+23k UXYH5 110-175

On the chart below, it makes sense as a profit-taking exit. I’m not much of an Elliott wave analyst, but it looks like the completion of a 5th wave up. 1st from late June to early August, 3rd from mid-August to late Sept, and 5th from early Dec to now. In any case, I checked prelim open interest and sure enough, TU fell 57k contracts. However, UXY prints UP 22k. More surprising than that, TY open interest jumped 143k contracts. It’s up 222k contracts since January 13, to 4.884 million. By the way, total SOFR OI was down 97k.

–There were no huge catalysts yesterday, though Waller said 3 to 4 eases could be appropriate this year if data cooperates. Not much reaction; SFRH5/H6 was around -24.5 when he spoke, and settled -28.5, which is more like 50/50 chance of 2 more eases over that time frame. Ten -year yield fell 5 bps to 4.602%.

–In any case, the last time we had a huge surge in open interest in TY (that wasn’t related to option expiration) was last summer. On June 21 OI was 4.33m and by August 21 it was 5.45m. Of course, there was a huge price surge related to yen-carry unwind and a weak NFP of 114k on 2-Aug. The ten-year yield went from 4.16% on July 1 to the low of 3.60% in mid-Sept. We’re now 4.60%. Is there something big going on behind the curtains?

–In SOFR there’s consistent buying of SFRZ5 call spreads. On Wednesday, Z5 9650/9700cs 8.25 paid around 40k and yesterday Z5 9637.5/9687.5cs 10-10.5 for 30k. Not really huge, but I always remember just before covid hit, someone was inhaling 50 bp wide call spreads in eurodollars. For some reason I recall as EDU0 9837.5/9887.5c spreads, but I’ll have to look it up later.

–What now? Yuan devaluation? Fed stops QT and pivots to QE? Bird flu? Vol isn’t super cheap in treasuries, but I do not want to be short it. The buyer of TY 108.5 and 109c delta neutral the last couple of days (150k) is perhaps onto something!

–News today includes Housing Starts. Half-day on screens in futures on Monday for MLK Day. Inauguration.

BOJ next week:

*MAJORITY OF BOJ BOARD MEMBERS TO FAVOR JAN. RATE HIKE: NIKKEI

Bob Uecker passed. They used to make pretty good beer commercials….

Covered call buyer adding in TY

January 16, 2025

******************

–Yields imploded on a slightly softer than expected Core CPI of 0.2% vs 0.3 exp and y/y 3.2% vs 3.3 expected. Curve flattened. 10y yield down 13 bps to 4.653%. 2y yield down almost 10 at 4.262%. Headline CPI yoy was 2.9% from 2.7% last. Not close to Fed’s target, but the market heaved a sigh of relief and shorts were covered.

–On the SOFR strip, greens (3rd year forward) were strongest, +16.75. Prices on red, green and blue packs (2nd, 3rd and 4th years) are still all nearly the same, just over 4%. Reds 9599.75, Greens 9590.5, Blues 9581.75. I saw a clip that Morgan Stanley is calling for an ease in March. Near contracts are underpriced if that were to occur. For example, FFG5 settled 9567.5, with just 0.5 premium to Fed Effective of 4.33. FFJ5 (April) is after the 19-March FOMC and is a clean month (no FOMC) priced at 9574.5. A cut would put Fed Eff at 4.08 or 9592. One-year calendars in SOFR declined as deferred contracts rallied harder. SFRH5/H6 settled exactly at -25; one ease over that year. (9577.5/9602.5).

–My thesis is that yesterday’s move was a short cover rally, typically associated with a decline in open interest. Indeed, SOFR OI dropped 141k in total. Main drops in M5 -41k (9590, +6.0), Z5 -32k (9602, +10.5) and Z6 -26k (9596.5. +16.0). In treasuries, TU -34k, FV +6k, US -19k, WN -3k. However, the ten-yr contract added open interest of 34k yesterday and 79k in the past two sessions. I attribute this to the big covered call buyer. On Tuesday, +100k TYH 108.5c around 28 covered ~107-10, 30 delta. So that added 30k contracts. By the way, at settle the calls were up 21/64s at 49 and the futures up just over a point, Per 1k, +10500/32s and -300*32.5/32s or -9750/32s. As of yesterday’s close, delta on 108.5c was 47.

Yesterday he continued, buying 40k 109c for 35 covered 108-09, 36 delta. So there’s another 14.4k futures. If he adjusted the hedge on the 108.5c he added around 15k short futures. TYH5 109c settle 36 vs 108-105.

Vol was down on the day with TYH5 108.5^ settling 1’45 or 6.2. Previous day atm 107.5^ was 1’51 or 6.5.

–In SOFR, notable buyer 40k SFRZ4 9650/9700cs for 8.25 (settled there ref 9602s)

–Retail Sales today expected +0.6 for Dec. Philly Fed -5.0 expected vs -16.4 last. Jobless Claims 210k. BOJ next week (hike expected).

–Beige book is old news, but sounded a bit muted. Going into the new Trump era, incentives are going to change dramatically, as evidenced by NFIB surge, Hamas/Israel deal, etc. Below from Beige Book:

Construction activity decreased overall, with several Districts indicating that high costs for materials and financing were weighing on growth. Manufacturing decreased slightly on net, and a number of Districts said manufacturers were stockpiling inventories in anticipation of higher tariffs. Residential real estate activity was unchanged on balance, as high mortgage rates continued to hold back demand.

Below is TY rolling in while, Aggregate Open Interest in blue. 100 dma in green.

Bonds remain weak going into CPI

January 15, 2025

******************

–Steeper curve yesterday with some large TY option trades going into today’s CPI data (more below). 2s fell 3.6 bps to 4.36% while 10s were down 1.4 to 4.784%. On the SOFR strip SFRZ5 was strongest +4 at 9591.5 (also peak price). Net changes tailed off from there. SFRZ6 +3 at 9580.5, Z7 +1.5 at 9570.

–TY option trades below. CPI expected +0.4 from 0.3 with Core 0.3 from 0.3. On yoy, 2.9 vs 2.7 and Core 3.3 from 3.3.

These figures are well above Fed targets, of course. In his last speech Waller mentioned ‘imputed’ prices, like those associated with housing, and said the trend was definitely lower if those prices are omitted. Given the loss of housing in LA, imputed prices might become more important again. Bank earnings kick off today: JPM, WFC, Citi, GS.

–PPI yesterday was lower than expected with Core m/m 0.0 vs expected 0.3 and y/y 3.5 vs 3.8. Stocks responded with an immediate knee-jerk higher (which faded) but bonds just can’t seem to get off the mat. Ultimately, TY settled 107-115, +4 and USH 110-29, +2. 30y bond yield pegged near 5%.

–Very near contracts have little fear of a pop in inflation which would cause a Fed response. For example, SFRH5 9568.75/9575 p 1×3 settled at POSITIVE (6.0/1.75 so 0.75, 1 leg over). 9575/9581.25 c 1×3 settled -6.25. 9575c settled 5.0 and the 9581.25c settled 3.75. The puts which are 5.25 otm are 1.75 and calls that are 7.25 otm are more than double that premium at 3.75.

–Huge buy on the day of 100k TYH5 108.5c for 27, 28, 29 covered 107-085, 10 and 11 (~30d). Open interest +98k in calls and 47k futures. There are some big long put positions, a lot in the 107.5 strike both Feb and March. There was a seller of 40k TYH5 106p covered 107-115/12 at 25 down to 24. Settled 25, open int in that strike fell 18k. Obviously there have been large shorts taken through puts in TY, and yesterday there were adjustments. But the covered call buying is not particularly bullish. On a hard break vol would probably move higher. On the upside, vol likely comes out but if the move is large enough gamma will help.

–Just a reminder that Chicago, and every other big city in US, can be dangerous:

Explosives found in Chicago South Side high-rise apartments HVAC worker finds “I came across some C4, some explosives, a rifle, A LOT OF FAKE IDs, a lot of fireman stuff, a lot of police force stuff, it was fake”

If neutral is lower, why are real yields going higher

January 14, 2025

******************

–USH5 contract made a new low 110-25. The low for the front US contract in October 2023 was 107-04. On the cash 30y bond, the high yield in October 2023 was 5.115%. I marked 4.984% at the time of futures settlement USH5 110-27. Worth noting is that the 30y inflation indexed note made a new high (real) yield of 2.603% just edging out the 2023 high of 2.582%. Chart attached. Slight new high 10y treasury/tip breakeven at 246.8 bps.

–Stocks rebounded modestly from early weakness (and follow-thru short cover rip overnight). There were a couple of large outlier trades: Buy of 50k TYG5 116.75c for cab-7. Buyer 12k SFRG5 9668.75/9700cs for 0.25. Disaster insurance; maybe the LA wildfires create focus on the unlikely. Buyer of 10k TYG 106/106.5 put stupid for 17 appears cover. Settled 18 (12 & 6).

Also a buyer of 40k SFRU5 9587.5/9606.25cs vs sell 9525p for -0.5 to +0.25. SFRU5 settled 9586.5. Great trade in my opinion though there will likely be a chance to enter better level. Option settles 26.5/20.75 and 5.5 so +0.25. Also a buyer 30k 0QH5 9606.25/96.3125c 1×2 for -0.25 to 0.0 (12.0s/6.0s). This looks good on paper…. until something really bad happens.

–Bank earnings: Wednesday JPM, WFC, C, GS and Thursday BAC, MS, USB, PNC.

Data: NFIB Small Biz Optimism expected to continue its rebound at 102.1. PPI 3.5% yoy vs 3.0 last. Core 3.8 from 3.4. CPI Wednesday 2.9 from 2.7 yoy. Then Retails Sales Thursday.

–DOGE in China? (RTRS)

Exclusive: China to cut pay by half for staff at top financial regulators, sources say

January Resolutions in Turmoil

January 13, 2025

******************

–January 10 was Quitter’s Day. The second Friday in January is apparently when most resolutions go out the window. If the resolution was ‘support financial assets’ then indeed, it seems to have crumbled.

–Yields soared on Friday’s blowout +256k payroll number. Curve flattened, giving back some of the steepening seen over the previous several sessions. On the treasury curve, 5s were weakest, jumping 12.7 bps in yield to 4.59%. Tens rose 8.1 to 4.772%. On the SOFR strip, reds were weakest, down 18.625 to 9583.625, greens -16.375 to 9574.88. blues -12.875 to 9569.125. Peak contract is now SFRZ5 at 9588.5, a yield of 4.115% which is less than one-quarter percent lower than the current SOFRRATE of 4.30%. I.e, not much easing being priced going forward.

–The lowest most inverted one-yr calendar is SFRH5/H6 at -12.5, up a whopping 13 bps Friday with SFRH5 down 5 to 9575 and H6 down 18 to 9587.5. In mid-September, just before the ease of 50 at the FOMC meeting, the Sept’24/Sept’25 spread was -203 bps. Of course, there was an actual reduction of 100 bps since then. (At the time, on 9/11, SFRZ4 was 9585 and SFRH25 was 9652.5.

–Starting out Monday with a lot of volatility. CLH5 up 1.25 at 77.00. On a continuous chart it’s around the high of early October, with press reports citing renewed sanctions on Russian oil. The British pound is in freefall, now 1.2124 (high at end of Sept was just over 1.34. Starmer said ready to sack Reeves). ESH5 is down 47, a new low for the move and testing early Nov low of 5796.5. Bitcoin is around 91k, a slight new low with prices appearing to have formed a head & shoulder formation which should target 74k, right at the 200 dma of 73569. SOFR contracts marginally lower, TYH5 printing a new low 107-09, down 3/32’s.

–Economic news includes the Fed’l Budget expected -$73.8b. CA wildfires will be a drain on the budget going forward, with current estimates of damage >$150b.

Luxury watch market in continuous decline, down about 15% over the past 2 years