Shifting Sands

December 9, 2024

*******************

–NFP about as expected at 227k (220k exp). However, Private payrolls were 194k vs 205k expected. So government payrolls rose, but they will be under the cutting knife next year. The Unemp rate upticked to 4.2%, enough to solidify expectations of an ease at the Dec 18 FOMC.

–Current EFFR is 4.58%. SOFRRATE has been 4.56 to 4.60 since the Fed cut on Nov 7. FFZ4 settled 9551.0, +1.25 (should end at 9552.5 on an ease). FFF5 settled 9564.0, +3.5. If the Fed eases 25 in Dec and holds off on Jan 29, then FFF5 would settle 9567.0 or 4.33%. FFG5 settled 9571.5, +4.5. So if 4.33 becomes the new EFFR, then this contract is indicating around a 20% chance of another cut in Jan. Does that make sense? If it does, then EFFR would be 4.08% going into the start of the Trump admin.

–Recent inflation levels: PCE yoy 2.3%, Core PCE 2.8%, CPI 2.6% (expected 2.7 on Wednesday). In this environment a real Fed Effective of 1.4% hardly would seem restrictive.

–Tectonic shifts over the weekend. Syria collapsed. China’s politburo eased, announcing it will embrace a “moderately loose” monetary strategy in 2025 (BBG) and will be “more proactive” on fiscal policy, pledging to “stabilize property and stock markets”. In short, a carbon copy of US policy. A politburo put. Hang Seng popped. China’s 10y yield hit a new low of 1.93%. It started the year at 2.57% and has slid lower without a significant retrace except for late Sept (from 2.04 to 2.21).

–South Korea’s Yoon is now forbidden to leave the country. The Korean Won is near the low of 2022 (level 1445) at current 1432. KOSPI at new low for the year. Theoretical question for US investors: can political upheaval actually cause selling in equity markets? Answer: sure, but not here. See Politburo (and Fed) policy above.

Low MOVE underpricing uncertainty

December 8, 2024 – Weekly comment

****************************************

Image below is MOVE (treasury vol index) and the yield of the US 10 year. The ten-year yield bottom corresponded with the September 18 FOMC 50 bp rate cut. That yield was 3.62% on September 16, the low for this calendar year. Rates soared from there going into the election, with Druckenmiller, Paul Tudor Jones and others warning about government bond supply associated with unsustainable deficit spending. The MOVE index firmed to the high of this calendar year (136 on Nov 4) on the back of put buying. Since the election, MOVE index has collapsed to 83.2, near the low of the year. The 10y yield has pulled back from 4.45% to 4.15%.

Friday’s employment report was a case in point. On Monday TYH5 settled 111-03+. TYH5 111 straddle settled 2’43. TYH5 110p settled 0’55 and the 112c at 0’60. On Friday TYH5 settled 111-145 and March 111.5^ at 2’29. On Friday, the 110p settled 0’41, down 14/64s from Monday’s price, and 112c 0’62, up 2/64s. Thursday to Friday change in 112c was just 3/64, half the move the delta would have indicated. Obviously the play was to be short puts.

There had been a buyer of 25k TY wk2 112c on Thursday for 10. Settled 8 on Friday despite the rally (futures +8.5/32s).

As a friend likes to say “How ya left?”

A few observations. First, the debt situation is not over, however my bias tilts toward a strong chance that the new administration is going to be successful in bending the spending trajectory lower. Vol has been taken down to levels that are a much better buy than sale. From here, I would prefer being long puts on long-dated treasuries. VIX at 12.77 Friday is lowest since July. Also a better buy than sale, though the VIX futures curve reflects that sentiment. Dec settled 14.28. Jan 15.95 and Feb 16.75.

After Waller said on Monday his lean was still for a December ease, and Powell stuck to middle-of- the-road comments on Wednesday, Friday’s increase of the unemployment rate to 4.2% was enough to solidify market expectations of a 25 bp cut at the Dec 18 FOMC. FFZ4 settled 9551.0, close to what should be the final settle on a cut ( 9552.5). If there’s a cut, EFFR will move down to 4.33% against CPI of 2.6 (with 2.7% expected Wednesday). Not sure where neutral is, but in this environment a real rate of 1.6 to 1.7% doesn’t seem particularly restrictive; probably not much room or urgency to cut much further unless employment and inflation data begin to crater.

Of course, global political upheaval could easily crush confidence. Currently SFRM5 settled 9609.5 or 3.905%. Option pricing shows that fear is still to the upside, as further otm calls trade at higher premiums than puts. The experience post-SVB hammered home the risk of being naked short otm calls.

SFRM5 9609.5

M5 9650c 14.0s delta= +29

M5 9575p 9.5s delta = -27

M5 9700c 7.25s delta = +15

M5 9525p 2.25s delta = -8

This week’s central bank meetings include: RBA on Monday (nothing expected) BOC on Wednesday (leaning 50) and SNB, ECB on Thursday (cut of 25 to 50). FOMC is on the 18th (25 expected) and BOJ on the 18th (small hike).

ERZ4/ERH5 3 month calendar settled -66 bps Monday (9718.5/9784.5) but popped up to -58.5 by the end of the week (9717/9775.5). A three-month calendar sub-50 is, of course, an indication of aggressive near term ease expectations.

OTHER THOUGHTS

Rapid collapse of Syria and even the United Healthcare CEO murder underline security concerns across various levels. Lotto ticket buy for rapid deterioration in global conditions: FVG5 111c settled 1.5/64s.

Treasury auctions this week:

TUES 3y, $58b

WED 10y, $39b

THUR 30y $22b

| 11/29/2024 | 12/6/2024 | chg | ||

| UST 2Y | 417.0 | 409.4 | -7.6 | |

| UST 5Y | 407.3 | 403.2 | -4.1 | |

| UST 10Y | 419.2 | 414.9 | -4.3 | wi 414.9 |

| UST 30Y | 437.8 | 433.0 | -4.8 | wi 432.9 |

| GERM 2Y | 195.7 | 200.0 | 4.3 | |

| GERM 10Y | 209.5 | 210.8 | 1.3 | |

| JPN 20Y | 185.2 | 185.9 | 0.7 | |

| CHINA 10Y | 203.3 | 195.2 | -8.1 | |

| SOFR H5/H6 | -49.0 | -44.5 | 4.5 | |

| SOFR H6/H7 | -10.5 | -6.5 | 4.0 | |

| SOFR H7/H8 | -2.0 | -2.5 | -0.5 | |

| EUR | 105.82 | 105.69 | -0.13 | |

| CRUDE (CLF5) | 68.00 | 67.20 | -0.80 | |

| SPX | 6032.38 | 6090.27 | 57.89 | 1.0% |

| VIX | 13.51 | 12.77 | -0.74 | |

| MOVE | 97.74 | 83.20 | -14.54 | |

Earth is Shaking

Dec 6, 2024

************

–Going into today’s payroll report (NFP expected 210 to 220k, rate 4.1) longer end contracts closed near the highs of the past week. TYH5 settled 111-065, down 1.5/32s, but well off the week’s low of 110-18. It feels like the market is set up a bit short, looking for a solid rebound in payrolls, but shorts were forced to pare back going into the data. Open interest in nearer treasuries fell, TU -14k, FV -52k, TY -24k, but UXY was +44k, US and WN had smaller changes which cancelled out.

–Large early sales of FFF5 and FFG5 : F5 35k at 9560.5 and G5 8k at 9566.5. Market leans toward ease at the Dec 18 FOMC, but these trades are a fade.

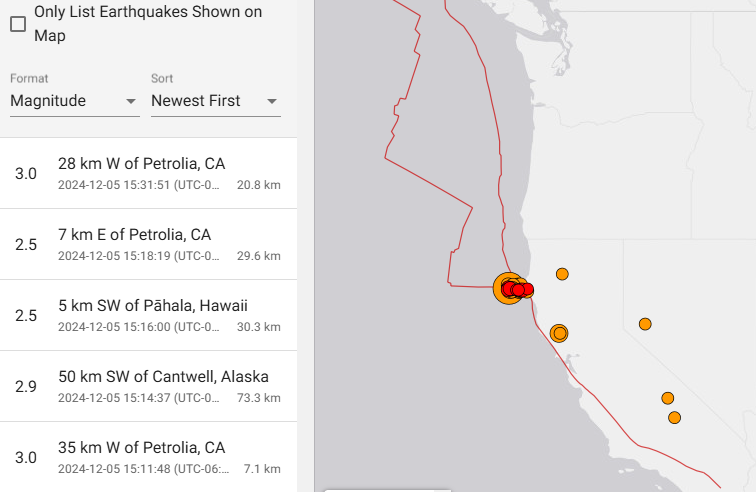

–Large earthquake off the northern coast of CA appeared to spark some buyers with warnings of a tsunami. Shortly after, buyer of 15 k SFRM5. U5 9650 c stupid 36.5 to 37.0. Settled 13 vs 9604 and 23.5 vs 9615.5. Later, a buyer of 25k TY wk2 (12/13) 112c for 10. Settled there ref 111-065. All of these buys are new.

–United Healthcare CEO was shot and killed in Manhattan. Stock ended -32 or 5.2%. Bond vigilantes aren’t quite as serious…

The three words were written on the ammunition a masked gunman used to kill UnitedHealthcare CEO Brian Thompson, according to two law enforcement officials who spoke to The Associated Press on condition of anonymity Thursday. They’re similar to the phrase “delay, deny, defend” — the way some attorneys describe how insurers deny services and payment, and the title of a 2010 book that was highly critical of the industry.

Front end pricing favors Dec cut

December 5, 2024

*******************

–News articles attribute bitcoin’s surge above 100k to a pro-crypto choice for the SEC. Paul Atkins. I guess it has nothing to do with political gymnastics in S Korea and France. Or with Blinken urging Ukraine to conscript younger kids into the meat grinder. Well, maybe it doesn’t because gold is still 5.5% off the high made just prior to the election. (Even priced in won, gold not quite at a new high). Bitcoin is easier to transport.

–Powell’s comments yesterday were middle of the road, though he said the US economy is in a good place and said it was stronger than the Fed had thought in September. Near contracts maintained a solid bid, with odds for a December cut increasing. SFRZ4 settled 9560, +1. FFZ4 settled 9549.75, 70-75% odds of a 25bp ease. FFF5 settled 9561.5, FFG5 9567.5s. Current EFFR is 4.58% or a price of 9542. A cut of 25 would take EFFR to 4.33% or 9567.0, exactly where FFG5 is now. On an actual ease on Dec 18, how much higher should FFG5 go? Depends on Fed guidance, but I doubt it could get to 50/50 (9579.5). Neutral is higher than they thought. Several Fed officials have tamped down on forward easing projections.

–New recent low in SFRH5/M5 three-month spread at -20.5 (9586, +3.5/9606.5 +5.5). Recent low in the spread was -38 on Sept 11 (pre-FOMC). Post-FOMC the spread rallied as all rate contracts sold off; recent high of -14.5 on Nov 22. The market believes Waller that the path of rates is lower over time, but the terminal rate has shifted higher. Peak contract on SOFR strip is SFRU7 at 9640 or 3.6%. SFRM5 is 9606.5…so there’s only 34 bps over that two-year period.

–Today’s news includes Jobless Claims expected 215k and Trade Balance. NFP tomorrow expected 200 to 215k; effects from Boeing strike and hurricane displacements still being felt. CPI is Wednesday.

Dec SOFR midcurves expire one week from tomorrow. SFRZ5 settled 9627.0 and 0QZ4 9625^ 19.5 (b/e 9644.5 and 9605.5). November range in Z5 was 9646 to 9601.5.

Just kidding about the whole ‘Martial Law’ thing…

December 4, 2024

*******************

–Early headline: URGENT: South Korean president declares emergency martial law, accusing opposition of anti-state activities South Korean President Yoon Suk Yeol declared an “emergency martial law,” Tuesday accusing the country’s opposition of controlling the parliament, sympathizing with North Korea and paralyzing the government with anti-state activities.

–UST went slightly bid but reverted lower as the martial law gambit quickly reversed. Curve was steeper by end of day. 2y yield fell 2.7 to 4.173% while tens were +3.1 to 4.225. From ending Monday slightly inverted, 2/10 finished Tuesday at +5.2 bps.

–JOLTS stronger than expected at 7744k. ADP today expected 150k from 233k ISM Services expected 55.7 from 56.0. Factory Orders and Durables as well. Beige Book in the afternoon.

–SFRZ4 9556.25/9568.75cs covered 9558 with 44d, 40k sold at 5.0. Appears exit settled 5.5 vs 59.

–Interesting post on X: THE NUMBER OF HOUSES FOR SALE IN FLORIDA JUST SKYROCKETED AND HAVE NEARLY DOUBLED IN THE PAST YEAR MANY OF THESE HOMES ARE AIRBNB RENTALS WITH OWNERS WHO ARE ABOUT TO DECLARE BANKRUPTCY DUE TO UNBEARABLE LOANS

https://twitter.com/MrMikeInvesting/status/1864107510132580787

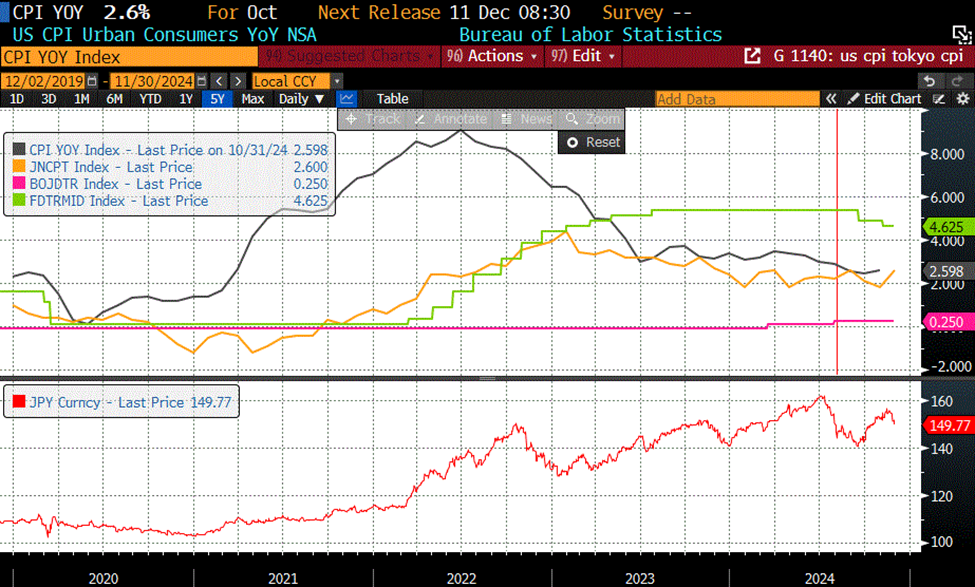

Linked-in post from weekend…$/yen

The FOMC is December 18. BOJ is December 19. On Friday (11/29) Ueda said the time for a hike is “approaching”. According to several articles, the probability of a hike is around 60% from the current 0.25% rate. (3m TIBOR fixing has moved from just above 25 bps to 36 bps since early November). On Thursday $/yen was 151.50, and after Ueda’s interview was published on Friday it touched 149.47.

The chart below shows US CPI in black, Tokyo CPI in amber, US FF midpoint in green and Japan’s base rate in pink. $/yen is in lower panel. According to these measures, inflation in both Japan and the US is 2.6%. The US FF mid is 200 bps above, and Japan’s base rate is 235 bps below. In terms of ‘recalibration’ it would appear more urgent on the side of Japan.

My guess is that the Fed will stand on the sidelines rather than ease, and that the BOJ will hike.

Why the emphasis on Japan? The red vertical line on the chart above shows the last BOJ hike. The yen had already been strengthening, from over 161 in early July to 150 by the end of the month. BOJ hike was August 5; $/yen hit 141.70 on the panicked unwind of yen-carry positions. In early July when $/yen was 161, SPX was around 5630. On August 5, the low was 5920, 5% lower. Over the same timeframe VIX exploded from 13 to 38. MOVE went from 94.8 on July 24 to 121 on August 5. Conditions became volatile. Of course, the monetary authorities immediately assured us that everything was going to be just fine, and that was the low for SPX.

The chart below shows $/yen in lockstep with the US 10y treasury yield since the beginning of August, and even prior there is a high degree of correlation. Since Nov 14, $/yen has moved from 156.50 to Friday’s low 149.50. The 10y yield has cratered from 4.45 to Friday’s 4.17. The pattern is similar to the period leading up to the BOJ’s last hike. Also similar is SPX blithely rallying into the possibility of choppy seas.

What if the US cuts and Japan hikes? $/yen to sub-145? Ten year yield sub-4%? A 5% sell-off in SPX would lead to the horror of 5730. Sure, that would be above every price since late September, but can we really all live with a year-over-year gain of just 20%? Shudder.

Waller reverses front-end weakness

December 3, 2024

*******************

–Early trades featured pressure on nearer contracts. For example, early buyer:

FV wk1 106.75p cov 107-12, 18d 5 paid 50k (Settled 3.5 vs 107-167, OI +53k).

FV wk 2 106.75p cov 107-12, 25d, 9.75 avg paid 35k (settled 7.5, OI +35k).

(likely large asset mgr protecting against possible BIG rebound in NFP Friday)

SFRZ4 9562.5c about 30k sold on the day at 2.0, settled 1.75, open int rose 32k.

SFRZ4 outright 30k sold at 9556, settled 55.5. Front end rather weak, with FFG5 down 3 to 9562.0.

–Pressure on front end led to curve flattening. 2y yield up 3 bps to 4.20% while tens were essentially unch’d at 4.194%; 2/10 slightly inverted again. 5/30 at bottom of recent range, +26.6. SFRH5/H6 edged to new low at -49.5 (9576, -3.5/9625.5 -3.0).

–However, Waller’s speech post-settle included these lines:

I expect rate cuts to continue over the next year until we approach a more neutral setting of the policy rate.

…at present I lean toward supporting a cut to the policy rate at our December meeting.

–SFRZ4 immediately popped to 59.5. FFG5 this morning has erased yesterday’s deficit and is printing 9565.0. No mention by Waller of equity prices and their impact on financial conditions (new all-time-high AAPL yesterday). My sense is that the Fed will hold pat in deference to BOJ (likely to hike) because the Fed would rather not re-live August 5 volatility associated with yen-carry trades. $/yen currently 150. A Fed ease and BOJ hike might risk 145… Yesterday SFRZ4 9556.25/9550ps settled 2.75, 30 minutes post-settle it was 2.0 offer.

–Kugler speaks today at 12:35 on labor markets and econ outlook. JOLTS this morning expected 7519k from 7443. Steady trend lower since the peak of 12182 in March 2022. It’s now around pre-covid 2019 level.

–A few more comments from Waller below:

It is also a reminder that there is still some distance to go in reducing the policy rate to neutral.

Now let me turn to the implications for monetary policy based on my assessment of the underlying economic outlook. While some near-term aspects of the outlook may be a little unclear, something that is clear is the direction for monetary policy and our policy rate over the medium term, which is down. This downward trajectory reflects the fact that the level of aggregate demand in the economy, relative to supply, has moderated significantly over the past year—it is plainly visible in the data on spending and the labor market.

https://www.federalreserve.gov/newsevents/speech/waller20241202a.htm

NFP Friday. ISM Mfg today. China 10’s below 2%

Dec 2, 2024

************

–Quiet day on Friday with yields slightly lower. Tens ended at 4.192% down 5.4 bps, and TYH5 settled 111-06, adding to a recent bounce. Big news of the week is the Unemployment report, with NFP expected 195 to 200k. The press is running with a lead story of Biden pardoning Hunter as if there is some sort of surprise value there. Perhaps the re-opening of hostilities in Aleppo is more important?

–On Friday BOJ’s Ueda said the time for a rate hike is approaching, with high odds now being placed on the Dec 19 meeting, the day after the FOMC. $/yen hit a low under 149.50 on the release of his comments. Treasury yields have moved lock-step with $/yen.

–In the race for a sub-2% ten year yield, China edged out Germany, with the former just below 2% today, and the latter at 2.04. To be fair, bunds ended 2023 at 1.90 (high of the year 2.69). China on the other hand, ended 2023 at 2.57; that yield has slid all year. Germany/France 10y spread is is 85 bps, the highest since 2012 when Draghi stopped the bleeding with his “whatever it takes” phrase.

–Today’s news includes ISM Mfg, expected 47.6 from 46.5. Prices Paid expected 56 from 54.8.

–Friday featured new lows in some of the near SOFR one-year calendars, with H5/H6 -49 (9579.5, +2.0/ 9628.5 +4.0). In mid-July H5/H6 was -74.5. It rallied to around -50 going into the Fed ease in Sept (H5 rallied harder), and then pulled back to -68. From there it powered to a high of -30.5 as red sofr contracts sold off hard in the wake of a perceived ‘mistake’ by the Fed in having eased too aggressively in Sept. Now -47. If growth measures of the new admin keep the Fed on the sidelines, sofr calendars will rally as reds converge toward front contract prices.

Labor side of dual mandate this week

December 1, 2024 – Weekly comment

****************************************

Yields plunged last week. I marked 5’s down 21.3 bps to 4.073%, 10s down 21.4 to 4.192% and 30s -21.6 to 4.378%. On the SOFR strip, every contract from SFRM6 to SFRM8 was up 21 to 21.5 bps. The prices: SFRM6= 9633.5 or 3.665% to a high on the strip of 9641 for U7, Z7 and H8 (3.59%). SFRM8 settled 9640.5 or 3.595%.

The big news items revolve around Bessent as choice for Treasury Sec’y, Tariffs with a capital T, and DOGE. Are yields declining because money is flooding into the US? DXY actually fell by 1.7% this week, but that was just a small retrace of the surge since October. The equation for GDP is C + I + G + (X-M). Consumption plus Investment plus Government plus (Exports minus Imports). G appears poised to fall. (X-M) is also at risk. A change in the composition of national income could easily make the Fed sit on their hands, to see how things shake out. According to the St Louis Fed site, Federal Net Outlays as % of GDP were 22.1% as of 2023. From 1992 to 2008 that number was 21% or lower, with a low of 17.5% in 2000.

Marc Andreesen was on Rogan and said that half of federal government workers have never returned to the office. (I have no idea if true). He said there’s one agency, where the union representing Federal Employees negotiated a deal that employees are required to come to the office just one day each month, so employees come in on the last day of the month and first day of the next month…2 days in 60 days…many have moved to cheaper locales. “DOGE announced you can work from home, just not for the Federal Gov’t.”

Or are yields declining because of generally softening conditions?

News this week includes ISM Mfg Monday. JOLTS on Tuesday, expected 7470k from 7443k. ADP Wednesday along with ISM Services. Beige book in the afternoon. Payrolls on Friday, expected 200k from 12k.

JOLTS has trended lower since the peak 12182 in March 2022. Last month’s 7443 was the lowest since early 2021 and is below the pre-pandemic level of early 2019. NFP at 12k last month was also lowest since Covid. The unemployment rate has been 4% or lower from late 2021 to June of this year. Now 4.1% with a recent high of 4.3%. Expected at 4.1 on Friday.

Having had a strong rally from end-of-June (-50) to end-of-September just after the Fed’s 50 bp ease (+22), 2/10 treasury spread has pulled back to 1.3 bps. Not exactly foreshadowing a restrictive Fed, but not loose either. The astounding 46% rally in the KRE regional bank index from late June to this week could easily see a pullback if the curve re-inverts. The positive aspect of lower regulation may collide with stingier liquidity from the Fed. From the Fed minutes last week: “A few participants discussed vulnerabilities posed by the growth of private credit and potential links to banks and other financial institutions.” Having missed SVB, perhaps the Fed will lean against the idea of a softer regulatory environment.

Putin last week:

Energy resources on the US market in some states are 3-5 times cheaper than in Europe and Germany. Entire enterprises, entire industries are shutting down in Germany and moving to the US. And they do it purposefully. But Americans are pragmatic people. Actually maybe they do the right thing in their own interests. But these [Germans/Europeans] it seems that if they’re told “we will hang you” they will have just one question “Should we bring the rope ourselves or you will give us one?” That’s it. So VW is shutting down, metallurgical companies are shutting down, chemical companies are shutting down, glass companies are shutting down. Hundreds or even thousands of people are being thrown out onto the streets.

The German bund ended the week at 2.09%, having been as high as 2.445% on Nov 7. Since the very beginning of 2024, this is the lowest yield apart from a spike down to 2.036% on October 1. Chart shows German bund, China 10y and Japan 20y, all closing in on 2%.

OTHER THOUGHTS/ TRADES

Below is a chart of the green SOFR pack, three years forward. Currently, it’s the average of SFRZ6, H7, M7 and U7. Level is 9639.375 or right around 3.6%. Yellow line is midpoint of FF target range.

In the past couple of years greens have surged three times to 9700 or above, ~3%. Each move was followed by unwinding over several months, to 4% or a bit higher. The market is currently near the midpoint, weighing fears of a slower labor market vs a growth spurt due to relaxed regulation/taxes, overlaid with concerns about massive debt issuance. The trend into year-end seems to support higher prices, lower yields. Friday’s data could have a large impact.

| 11/22/2024 | 11/29/2024 | chg | ||

| UST 2Y | 434.4 | 417.0 | -17.4 | |

| UST 5Y | 428.6 | 407.3 | -21.3 | |

| UST 10Y | 440.6 | 419.2 | -21.4 | |

| UST 30Y | 459.4 | 437.8 | -21.6 | |

| GERM 2Y | 199.1 | 195.7 | -3.4 | |

| GERM 10Y | 224.2 | 209.5 | -14.7 | |

| JPN 20Y | 189.0 | 185.2 | -3.8 | |

| CHINA 10Y | 208.0 | 203.3 | -4.7 | |

| SOFR Z4/Z5 | -51.0 | -63.3 | -12.3 | |

| SOFR Z5/Z6 | -12.5 | -17.0 | -4.5 | |

| SOFR Z6/Z7 | -3.5 | -4.0 | -0.5 | |

| EUR | 104.18 | 105.82 | 1.64 | |

| CRUDE (CLF5) | 71.24 | 68.00 | -3.24 | |

| SPX | 5969.34 | 6032.38 | 63.04 | 1.1% |

| VIX | 15.24 | 13.51 | -1.73 | |

| MOVE | 99.14 | 97.74 | -1.40 | |

Bond differentials don’t matter, then they do

November 29, 2024

*********************

–Wednesday featured thin conditions. PCE prices exactly as expected with yoy 2.3% and Core 2.8%. Yields ended lower on the day, with tens down 5.8 bps to 4.246%. Ten year inflation-indexed note to treasury marked at a new recent low of 228 bps (exactly at yoy PCE). Treasury to tip spread this year has ranged from a high high of 243 in April to a low of 203 in early Sept, just prior to the FOMC. Fairly well anchored. High this month is 240.

–A few near SOFR one-year calendars made new lows, for example SFRH5/H6 now -47 (9577.5, +3/ 9624.5 +7). Every three-month spread from Dec’24 forward is inverted until U7/Z7 which is zero (9637/9637). Greens to blues slightly inverted, wouldn’t be surprised to see those pop back to positive, but a lot will depend on the Fed’s posture.

–Tokyo’s Core prices released today were higher than expected at 2.2% vs 2.1 expected. $/yen has fallen to 150 this morning from 151.50 yesterday. High on Nov 15 was 156.70. BOJ meeting is 19-Dec, with odds of a hike about 60% according to Reuters. I’ve attached a chart of 20y JGB to US. The spread is 261 bps and falling, with US 4.47% and JGB 1.86%. In the August yen-carry debacle, a fear was that rising JGB yields would siphon Japanese money back into the domestic market. US FOMC on Dec 18 is around 50/50 for a cut. Fed and BOJ swing by 50 bps?

–I’ve also attached an interesting chart of the French 10y vs that of Greece. Spread now zero. Do bond yields matter in terms of forcing fiscal discipline…or throwing it out the fenêtre? When Greece was considered a basket case, France was borrowing at zero (or negative). Now the tables have turned.

–Markets should be quiet today.