I’ve got an idea…

October 12, 2023

–CPI and 30y auction today. On y/y basis, CPI expected 3.6 vs 3.7 last and Core 4.1 vs 4.3. Social Security will reveal its COLA today, expected 3.2% for 2024, down from 8.7% last year and 5.9% in 2022. JPM, C and WFC report on Friday.

–Interesting bullet point from Waller yesterday:

When the deficit is 6% with low unemployment, it’s hard to see that as sustainable. Clearly issuance has to have an impact on yields.

–What’s the response from the braintrust at Treasury? Well according to a Barclay’s report (from a BBG piece in the morning):

Barclays predicts treasury is about to slow terming-out of debt. “Int rate strategists at Barclays said they expect the US Treasury to ‘slow the pace of terming out’ debt starting next month in response to a sharp increase in term premium and strong demand for bills.” …Slowing the treasury’s terming out could reduce term premium and flatten the curve.

–Oil high? Sell out of the SPR. Long rates high? Trim bond sales. Don’t have coal to heat the house? Burn the furniture. Idiots.

By the way, another gem from Yellen: She said the price cap on Russian oil had “significantly reduced Russian revenue over the last 10 months while promoting stable energy markets.”.(RTRS).

I guess we now characterize stable markets as selling Russian oil to India which is then purchased by Europe.

–The US curve did flatten aggressively yesterday, with 5/30 down to 13 bps from a new recent high of 21 on Tuesday. This, despite a 30 year auction today, which follows tailing results in both the 3y and 10y.

–I think the phrase, “This is going to end badly” is way overused and somewhat stupid, but appropriate here (and you can apply the last characterization to either the situation or the author regarding today’s missive).

–Large buying yesterday of SFRZ3 9468.75/9475/9481.25/9487.5 c condor for 0.25 (mostly) up to 0.5, about 50k. SFRZ3 9468.75/9481.25 c spread bought about 10k, synthetically from 0.65 to 0.75. SFRZ3 settled 9457.0. These trades require a strong expectation of ease in the former, and either that or an actual end-of-year ease in the latter.

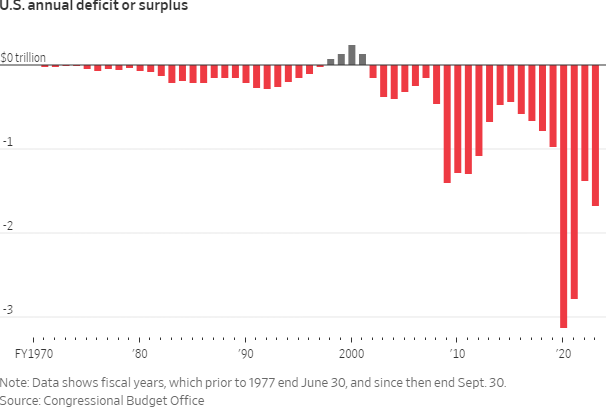

Here’s a stark picture of the US deficit from today’s WSJ. Below that is a Game of Trades post: Bank credit is now contracting. Has only happened once: in the GFC.

https://twitter.com/GameofTrades_/status/1712157718507901325/photo/1

bank credit contraction

..