Fed’s response to bad stuff pushed forward

August 16, 2022

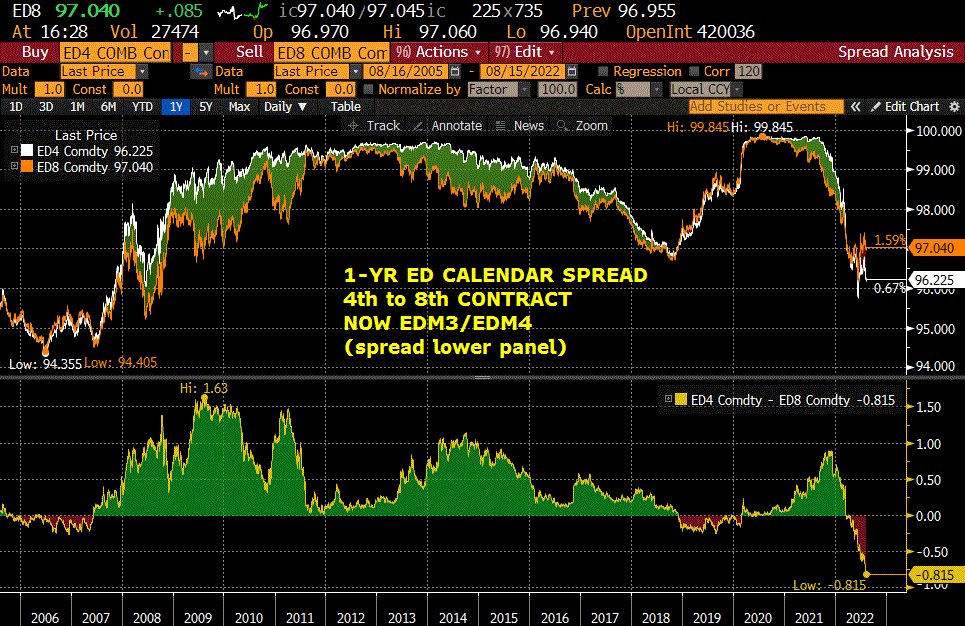

–Since the year 2000, the lowest ED one-year calendar was the 1st to 5th contract spread at the end of 2007, at -158 bps. Makes sense, the level of rates was high at the time (5.25% FF at the end of 2006) and it was becoming clear the Fed would have to cut hard. It’s typically the 1st/5th that inverts the most, as the market prices a near term pivot to easing. In 2019 the first to fifth contract spread got to -82.5 (lowest in the cycle). The situation is different now as inflation keeps the Fed on a front-loaded hike path. Currently the lowest one-year spread is nearly one year forward: EDM3/EDM4 settled -81.5, a new low for any 1yr this time around. The implicit forecast is that bad things will be happening in the economy by the middle of next year that will prompt Fed easing.

–Of course, there are already warnings on growth. China eased yesterday due in large measure to real estate woes. In the US, Empire State Mfg was -31.3 vs +5 expected, not only a miss, but a level equal to the lows of the GFC if not Covid. Same thing with NAHB; it was 49 vs 54 expected. Today we have Housing Starts (1528k expected) and Industrial Production at +0.3.

–I highlighted EDM3/M4 but the red pack to all deferred contracts edged to new lows; red pack to green pack settled -53.75. On the treasury curve there was flattening pressure early. which abated by the end of the day. 2/10 closed -41.1, up about 0.5. Commodities were crushed yesterday, with CLU hovering around $88/bbl late, down over $4 on the day.