Do Bond Yields Continue Higher?

January 12, 2025 – Weekly Comment

***************************************

I don’t believe the payroll data. However, there’s no doubt that the US economy has been resilient. In any case, the employment report (NFP 256k) bolsters the last Fed dot plot which ratcheted up inflation estimates. (PCE price estimate for 2025 in September was 2.1%, moved up to 2.5% in December). The bar has become quite a bit higher in terms of future Fed rate cuts.

Above is a chart of global bond yields. New highs in Japan and the UK; the trend has been higher for all Western bonds.

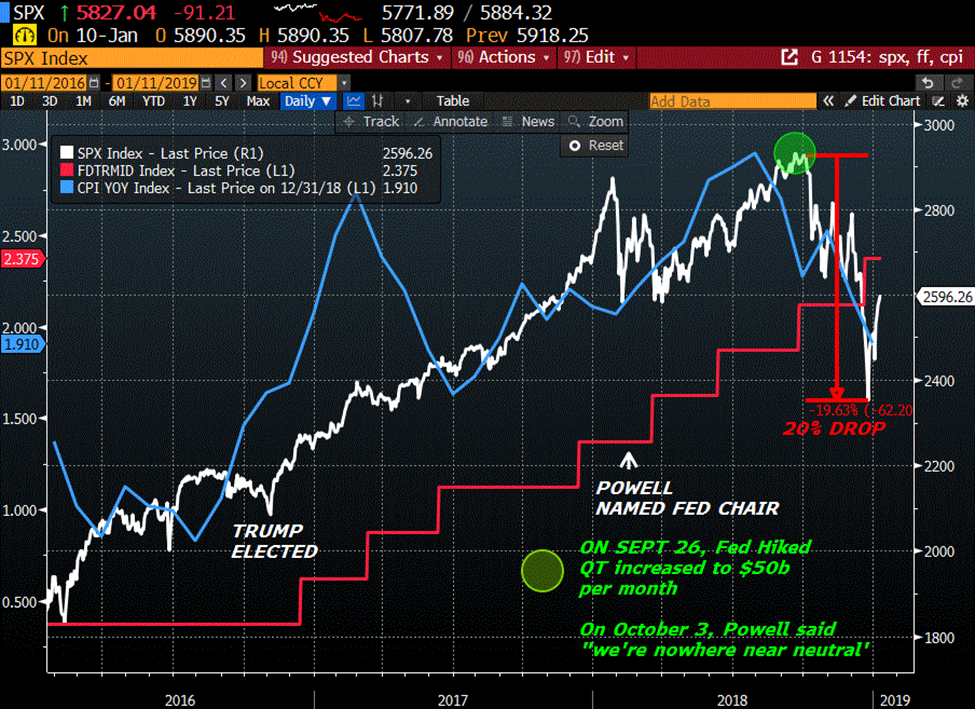

What happened in 2018 to arrest the rise in global bond yields? (Red rectangle on chart). What I recall was a 20% drop in SPX from the start of October 2018 to the end of the year. Janet Yellen had taken tentative steps to raise the FF target from 0.25% to 1.25-1.50% by the end of her term. Powell became Chair in Feb 2018. From March to the end of September, FF (midpoint) went from 1.375% to 2.125%. Not a particularly large move, but at the same time QT was ratcheting higher. At the June 13, 2018 FOMC, the amount being shed from the Fed’s balance sheet was $40 billion per month. At the Sept 26 meeting it was increased to $50 billion. On October 3, Powell said “We may go past neutral. But we‘re a long way from neutral at this point, probably.” That was the pin. I think this time it was the December SEP.

On the below chart I highlight 2016 to the end of 2018, the initial Trump years. Just a few select data series: SPX in white, CPI in blue, FF (midpoint) target in red. A couple of things to notice: From the election in Nov 2016 to Jan 2018 SPX rallied 37%, then corrected as the euphoria from the tax package was exhaled. Powell came in with the intent to ‘normalize’ rates. QT and rate hikes at the same time. Even though stocks cratered in Q3 2018, the Fed hiked one last time in December, finally bringing FF back above CPI. Global bond yields fell for the next year. By the way, CPI high in 2018 was 2.9%, now 2.7%. PCE yoy Prices were 2.3% now 2.4%. Core PCE 2.0% now 2.8%

So what’s going on now? With PCE prices at 2.4% and FF at 4.33%, an argument can be made that we’re at neutral now, or perhaps a shade high. Inflation expectations have been moving up, for example, ten yr breakeven (Treasury minus TIP) has gone from 205 bps to 245 since the Sept FOMC. The LA wildfires are likely inflationary while adding to gov’t budget woes, and have caused massive wealth destruction. That loss of wealth will be plugged to some extent by the Federal Gov’t further pressuring debt dynamics.

From WSJ:

A Harvard Business School study found that expensive disasters in some parts of the country affect insurance rates in others, as insurers bump up premiums for homeowners in other areas to help cover big losses.

Probably didn’t need to go to Havard to figure that out.

The dollar index is making new highs (since late 2022). I would note that DXY was in rally mode in 2018 as well. For me, the question is: IF we get a significant stock market sell off, will bond yields begin to reverse lower? So far SPX has had a minor pullback of 4.3% since the early Dec high. The August pullback associated with yen-carry unwinding was 8.5%. A similar magnitude move from the Dec high of 6090 in SPX would be 517 lower, or 5575 (vs Friday’s close of 5827). A 20% decline off the December high is ~4875, which would essentially erase 2024 gains.

One other note with regard to QT. From the start of 2018 to the low in September 2019, the Fed’s balance sheet declined $680b from $4.44T to $3.76T, about 15%. Since the high in April 2022 of $8.96T it has declined to a current value of $6.85T, or $2.11T, nearly 25%. For Fibonacci enthusiasts, we’re just over a 38.2% retrace of the 2019 low to 2022 high.

The third paragraph of the last Fed Minutes addressed the timing for the end of balance sheet runoff. Currently, total bank reserves are $3.255T, more than 10% above GDP, probably at the tipping point of ‘ample’. I believe discussions to end runoff will be brought forward in a more urgent way at the Jan FOMC. Third paragraph of Dec minutes:

The manager also discussed balance sheet policy expectations. The average estimate of survey respondents for the timing of the end of balance sheet runoff shifted a bit later, to June 2025. This shift mainly reflected revisions to estimates by respondents who had expected balance sheet runoff to end in the last quarter of 2024 or in early 2025.

***********

On the week, the 5y yield jumped 17.8 bps to 4.59%, 10s rose 17.3 to 4.772% and 30s 14.4 to 4.963%. On the SOFR strip, SFRH5 down 6 to 9575, H6 -15 to 9587.5, H7 -22 to 9577.5 and H8 -25 to 9571. Back SOFR calendars steepened through the week but then flattened Friday with the stark realization that Fed easing could be over. On Friday the biggest loser on the SOFR strip was SFRM’26 at 9585, down 19, while SFRM’28 was only down 13.5 to 9569.5.

While the MOVE index ended the week higher, vols declined on Friday, indicating that long-end panic is subsiding. In the past few months, many heavy-weight traders warned about the long end in the US (Druckenmiller, Paul Tudor Jones, Gundlach, etc). The short bond trade isn’t necessarily ‘crowded’ but 10y yields have surged 110 bps since the Sept FOMC and 50 bp cut.

Recall it was October 2023 when Ackman spectacularly called the top in yields. From CNBC ‘Bill Ackman covers bet against Treasury, says ‘too much risk in the world’ to bet against bonds’ Key points were “…investors may increasingly buy bonds as safe haven because of growing geopolitical risks.” And “Ackman…removed the short because of concern about the economy.” Tens topped at 5% on Oct 19, and are now ¼% away at 4.76%.

Do bonds blow up due to bad budget dynamics, or become a port in the storm due to wealth destruction?

| 1/3/2025 | 1/10/2025 | chg | ||

| UST 2Y | 427.9 | 439.2 | 11.3 | |

| UST 5Y | 441.2 | 459.0 | 17.8 | |

| UST 10Y | 459.9 | 477.2 | 17.3 | |

| UST 30Y | 481.9 | 496.3 | 14.4 | |

| GERM 2Y | 216.1 | 228.4 | 12.3 | |

| GERM 10Y | 242.5 | 259.5 | 17.0 | |

| JPN 20Y | 188.2 | 195.9 | 7.7 | |

| CHINA 10Y | 162.1 | 165.3 | 3.2 | |

| SOFR H5/H6 | -21.5 | -12.5 | 9.0 | |

| SOFR H6/H7 | 3.0 | 10.0 | 7.0 | |

| SOFR H7/H8 | 3.5 | 6.5 | 3.0 | |

| EUR | 103.09 | 102.55 | -0.54 | |

| CRUDE (CLH5) | 73.21 | 75.75 | 2.54 | |

| SPX | 5942.47 | 5827.04 | -115.43 | -1.9% |

| VIX | 16.13 | 19.54 | 3.41 | |

| MOVE | 96.67 | 99.73 | 3.06 | |