Sudden re-pricing

June 24, 2022

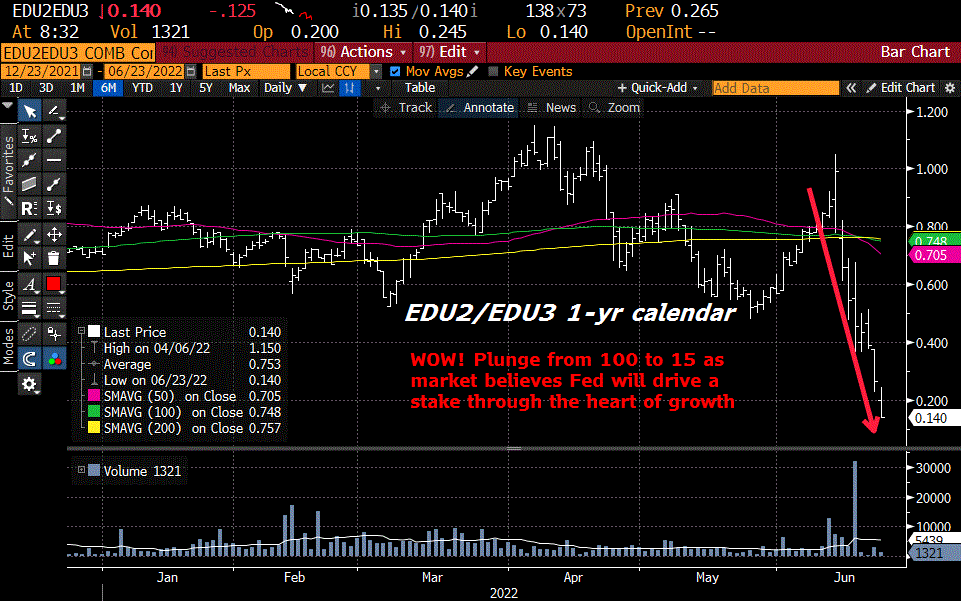

–Repricing since the FOMC meeting has been extraordinary. On June 15, the day of the meeting, EDU2/EDU3 settled 54.5. Yesterday it traded as low as 5 before coming back to settle 15.5. EDZ2/EDZ3 was -28.5 but settled -44 yesterday. EDZ2/EDH3 was 11, traded as low as -7.5 before settling -4.5 yesterday. The new pricing indicates that hikes end this year, followed by a strong bias towards easing next year (despite the Fed’s dot plot which forecasts continued modest hikes in 2023).

–Yields plunged yesterday morning, partially as PMI weaker than expected. EDU3 traded as high as 9672 before coming back to settle 9653.5. At the high the contract was nearly 100 higher than the low set just before the FOMC on June 13, which was 9580.5. At futures settle, the ten year yield was down nearly 10 bps to 3.065%. Exaggerated moves reflect both uncertainty and illiquidity.

–The price of copper and other base metals continues to plunge. HGN2 this morning is 3.72; it started the month around 4.50. The prices of economically sensitive inputs have dropped as calls for a slowdown have captured the narrative…having been telegraphed by the eurodollar curve months ago. Ten year treasury to inflation-indexed yield made a new low of 250 bps. Mexico hiked 75 bps to 7.75%. Inflation for Q3 is expected 8.1%, so that’s a rather restrictive policy rate, compared to the Fed’s dots which project year-end inflation at 5.2% with FF at 3.4%. In any case, higher market rates of interest have had an impact, likely to be reflected by today’s New Home Sales (for May) expected at a rate of 590k as compared to the start of the year around 840k.